[TO BE PUBLSIHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

[CENTRAL BOARD OF DIRECT TAXES]

(INCOME – TAX)

Notification

New Delhi, the 14th January, 2016

S.O. 127 (E).- In exercise of the powers conferred by section 11 read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax (1st Amendment) Rules, 2016.

(2) They shall come into force from the 1st day of April, 2016.

2. In the Income-tax Rules, 1962 (hereinafter referred to as the said rules), for rule 17, the following rule shall be substituted, namely:-

“17. Exercise of option etc under section 11. (1) The option to be exercised in accordance with the provisions of the Explanation to subsection (1) of section 11 in respect of income of any previous year relevant to the assessment year beginning on or after the 1st day of April, 2016 shall be in Form No. 9A and shall be furnished before the expiry of the time allowed under sub-section (1) of section 139 for furnishing the return of income of the relevant assessment year.

(2) The statement to be furnished to the Assessing Officer or the prescribed authority under sub-section (2) of section 11 or under the said provision as applicable under clause (21) of section 10 shall be in Form No. 10 and shall be furnished before the expiry of the time allowed under sub-section (1) of section 139, for furnishing the return of income.

(3) The option in Form No. 9A referred to in sub-rule (1) and the statement in Form No.10 referred to in sub-rule (2) shall be furnished electronically either under digital signature or electronic verification code.

(4) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall-

(i) specify the procedure for filing of Forms referred to in sub-rule (3);

(ii) specify the data structure, standards and manner of generation of electronic verification code, referred to in sub-rule(3), for purpose of verification of the person furnishing the said Forms; and (iii) be responsible for formulating and implementing appropriate security, archival and retrieval policies in relation to Forms so furnished.”.

3. In the said rules, in Appendix II,- (a) after Form No.9, the following Form shall be inserted, namely:-

“FORM NO 9A

[See rule 17(1)]

Application for exercise of option under clause (2) of the Explanation to sub-section (1) of section 11 of the Income – tax Act, 1961.

To

The Assessing Officer,

I, ,…………… on behalf of [name of the trust/institution/association]……………………. Permanent Account Number (PAN)……………………………….. do hereby wish to exercise the option referred to in clause (2) of the Explanation to sub-section (1) of section 11 of the Income-tax Act, 1961 for an amount of Rs…………………..( detailed in A below) to be deemed to be the income applied for charitable or religious purposes during the previous year 20..- 20.. for the reasons mentioned in B below.

A. The details of income in this regard are:

(i) Amount of income derived from property held under trust / held under trust in part, during the above mentioned previous year: Rs……………….;

(ii) Amount of income [out of (i)] actually applied to charitable or religious purposes in India: Rs …………………….;

(iii) Amount of income referred to in (ii) that falls short of 85% of the income referred to in (i) : Rs……………..;

(iv) The amount of income in respect of which the option is being exercised: Rs………………

B. The reasons for the shortfall in application of income are as under:-

(a)Whether the income was not received during the previous year? Yes/No.

If Yes, the amount of income that was not received:……………;

(b) any other reason ? Yes/No

If yes, then specify the reason and the corresponding amount of income:

Sr.No Reason for shortfall Amount of Income

Date:

Signature…………………………….

Designation………………………….

Address………………………………

Note: 1. This option Form should be signed by a trustee/principal officer.

2. Delete the inappropriate words.”;

(b) for Form No.10, the following Form shall be substituted, namely:-

“FORM NO.10

[See rule 17(2)]

Statement to be furnished to the Assessing Officer/Prescribed Authority under sub-section (2) of section 11 of the Incomer-tax Act, 1961

To

The Assessing Officer/ Prescribed Authority,

…………………………………………………

…………………………………………………

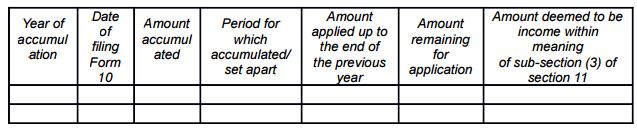

I, ,…………… on behalf of…………………………… [name of the trust/institution/association] Permanent Account Number ……………… hereby bring to your notice that it has been decided by a resolution passed by the trustees/governing body, by whatever name called, on…………………. that, out of the income of the trust/institution/association for the previous year, relevant to the assessment year 20….-20…., an amount of Rs…….. which is ………..per cent of the income of the trust/institution/association for the said previous year, shall be accumulated or set apart for carrying out the purposes of the trust/association/institution. The details of the amount, the purpose and period of the proposed accumulation or setting apart is as under:-

2. The amount so accumulated or set apart has been invested or deposited in any one or more of the forms or modes specified in sub-section(5) of section 11 of the Income-tax Act, 1961.

3. It is further brought to your notice that the said …………………. [name of the trust/institution/association] had in respect of an assessment year preceding the relevant assessment year given the statement regarding accumulation or setting apart of an amount as required under sub-section (2) of section 11 of the Income-tax Act, 1961 as detailed below:

4. It is also brought to your notice that , out of incomes detailed in 3 above, due to the order/ injunction of the court the income as detailed below could not be applied for the purpose for which it was accumulated or set apart:-

Date: ………………

Signature………………………

Designation……………….……

Address……………….………

Notes: 1. This statement should be signed by a trustee/principal officer.

2. Delete the inappropriate words.”.

Notification No.3/2016 /2015 [F. No. 142/16/2015-TPL]

(R LAKSHMI NARAYANAN)

Under Secretary (Tax Policy and Legislation)

Note: – The principal rules were published in the Gazette of India Extraordinary, Part II, Section 3, Sub-section (i), vide notification number S.O. 969(E), dated the, 26th March, 1962 and last amended vide notification number S.O- 3545 (E), dated the 30th December, 2015.