FREQUENTLY ASKED QUESTIONS

ON

SEBI (SUBSTANTIAL ACQUISITION OF SHARES AND TAKEOVERS) REGULATIONS, 2011

These FAQs offer only a simplistic explanation/clarification of terms/concepts related to the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 [“SAST Regulations, 2011”]. Any such explanation/clarification that is provided herein should not be regarded as an interpretation of law nor be treated as a binding opinion/guidance from the Securities and Exchange Board of India [“SEBI”]. For full particulars of laws governing the substantial acquisition of shares and takeovers, please refer to actual text of the Acts/Regulations/Circulars appearing under the Legal Framework Section on the SEBI website.

1. Please provide details as to how the regulatory framework governing Takeovers has evolved over a period?

- The earliest attempts at regulating takeovers in India can be traced back to the 1990s with the incorporation of Clause 40 in the Listing Agreement.

- While, the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 1994 which were notified in November 1994 made way for regulation of hostile takeovers and competitive offers for the first time; the subsequent regulatory experience from such offers brought out certain inadequacies existing in those Regulations. As a result, the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 1997 were introduced and notified on February 20, 1997, pursuant to repeal of the 1994 Regulations.

- Owing to several factors such as the growth of Mergers & Acquisitions activity in India as the preferred mode of restructuring, the increasing sophistication of takeover market, the decade long regulatory experience and various judicial pronouncements, it was felt necessary to review the Takeover Regulations 1997. Accordingly, SEBI formed a Takeover Regulations Advisory Committee (TRAC) in September 2009 under the Chairmanship of (Late) Shri. C. Achuthan, Former Presiding Officer, Securities Appellate Tribunal (SAT) for this purpose. After extensive public consultation on the report submitted by TRAC, SEBI came out with the SAST Regulations 2011 which were notified on September 23, 2011. The Takeover Regulations, 1997 stand repealed from October 22, 2011, i.e. the date on which SAST Regulations, 2011 come into force.

2. What is the significance of the notification related to SAST Regulations, 2011 published on September 23, 2011?

Vide the said notification dated September 23, 2011, the SAST Regulations, 2011 were notified to replace SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 1997, since repealed.. SAST Regulations, 2011 come into force with effect from October 22, 2011. SAST Regulations, 2011 are available on SEBI’s website under the section legal framework.

3. When the Takeover Regulations, 2011 have come in to force?

October 22, 2011 i.e. 30th day from the date of notification. (September 23, 2011 i.e. date of notification has been taken as the first day for computing 30 days).

4. What is meant by Takeovers & Substantial acquisition of shares?

When an “acquirer” takes over the control of the “Target Company”, it is termed as Takeover. When an acquirer acquires “substantial quantity of shares or voting rights” of the Target Company, it results into substantial acquisition of shares.

5. Who is an ‘Acquirer’?

Acquirer means any person who, whether by himself, or through, or with persons acting in concert with him, directly or indirectly, acquires or agrees to acquire shares or voting rights in, or control over a target company. An acquirer can be a natural person, a corporate entity or any other legal entity.

6. What is meant by Persons acting in Concert or ‘PAC’ in the context of SAST Regulations, 2011?

PACs are individual(s)/company (ies) or any other legal entity (ies) who, with a common objective or purpose of acquisition of shares or voting rights in, or exercise of control over the target company, pursuant to an agreement or understanding, formal or informal, directly or indirectly co-operate for acquisition of shares or voting rights in, or exercise of control over the target company.

SAST Regulations, 2011 define various categories of persons who are deemed to be acting in concert with other persons in the same category, unless the contrary is established.

7. What is a ‘Target Company’?

The company / body corporate or corporation whose equity shares are listed in a stock Exchange and in which a change of shareholding or control is proposed by an acquirer, is referred to as the ‘Target Company’.

8. What is an open offer under the SAST Regulations, 2011?

An open offer is an offer made by the acquirer to the shareholders of the target company inviting them to tender their shares in the target company at a particular price. The primary purpose of an open offer is to provide an exit option to the shareholders of the target company on account of the change in control or substantial acquisition of shares, occurring in the target company.

9. Under which situations is an open offer required to be made by an acquirer?

If an acquirer has agreed to acquire or acquired control over a target company or shares or voting rights in a target company which would be in excess of the threshold limits, then the acquirer is required to make an open offer to shareholders of the target company.

10. Can the acquisitions, resulting from any agreement attracting the obligation to make an open offer, be completed by way of transactions settled on stock exchange such as bulk/block deals?

No. Regulation 22(1) of Takeover Regulations 2011 specifically provides that the acquirer shall not complete the acquisition of shares and voting rights in, or control over, the target company, whether by way of subscription of shares or a purchase of shares attracting the obligation to make an open offer for acquiring shares, until the expiry of the offer period.

In cases where acquisitions, resulting from any agreement triggering open offer are sought to be completed through transactions such as bulk/ block deals, settled on a recognized stock exchange, the same would get completed/ settled on T+2 basis i.e. within 2 days after the date of such transaction. Therefore such acquisitions, if done, will not be in line with the provisions of Regulation 22(1) since the same would result in completion of the triggering acquisition before the expiry of the offer period. Hence the acquisition resulting from any agreement attracting the obligation to make an open offer cannot be executed through transactions such as block/ bulk deal.

11. What are the threshold limits for acquisition of shares / voting rights, beyond which an obligation to make an open offer is triggered?

Acquisition of 25% or more shares or voting rights: An acquirer, who (along with PACs, if any) holds less than 25% shares or voting rights in a target company and agrees to acquire shares or acquires shares which along with his/ PAC’s existing shareholding would entitle him to exercise 25% or more shares or voting rights in a target company, will need to make an open offer before acquiring such additional shares.

Acquisition of more than 5% shares or voting rights in a financial year: An acquirer who (along with PACs, if any) holds 25% or more but less than the maximum permissible non-public shareholding in a target company, can acquire additional shares in the target company as would entitle him to exercise more than 5% of the voting rights in any financial year ending March 31, only after making an open offer.

12. How is the maximum permissible non-public shareholding in a listed company defined?

Maximum permissible non-public shareholding is derived based on the minimum public shareholding requirement under the Securities Contracts (Regulations) Rules 1957 (“SCRR”). Rule 19A of SCRR requires all listed companies (other than public sector companies) to maintain public shareholding of at least 25% of share capital of the company. Thus by deduction, the maximum number of shares which can be held by promoters i.e. Maximum permissible non-public shareholding) in a listed companies (other than public sector companies) is 75% of the share capital.

13. What is the basis of computation of the creeping acquisitions limit under Regulation 3(2) of Takeover Regulations 2011?

For computing acquisitions limits for creeping acquisition specified under regulation 3(2), gross acquisitions/ purchases shall be taken in to account thereby ignoring any intermittent fall in shareholding or voting rights whether owing to disposal of shares or dilution of voting rights on account of fresh issue of shares by the target company.

14. Whether for the purpose of the creeping acquisition in terms of the Takeover Regulations, 2011, the Creeping Acquisition made during the period 01.04.2011 to 22.10.2011 will be considered?

The Takeover Regulations, 2011 have clearly defined the financial year as the period of 12 months commencing on the first day of the month of April.

Thus, for the purpose of the creeping acquisitions under Regulation 3(2) of Takeovers Regulations 2011, shares acquired during 1/4/2011 to 22/10/2011 will be taken in to account.

15. Whether hostile offers/bids are permitted under the new regulations?

There is no such term as hostile bid in the regulations. The hostile bid is generally understood to be an unsolicited bid by a person, without any arrangement or MOU with persons currently in control.

Any person with or without holding any shares in a target company, can make an offer to acquire shares of a listed company subject to minimum offer size of 26%.

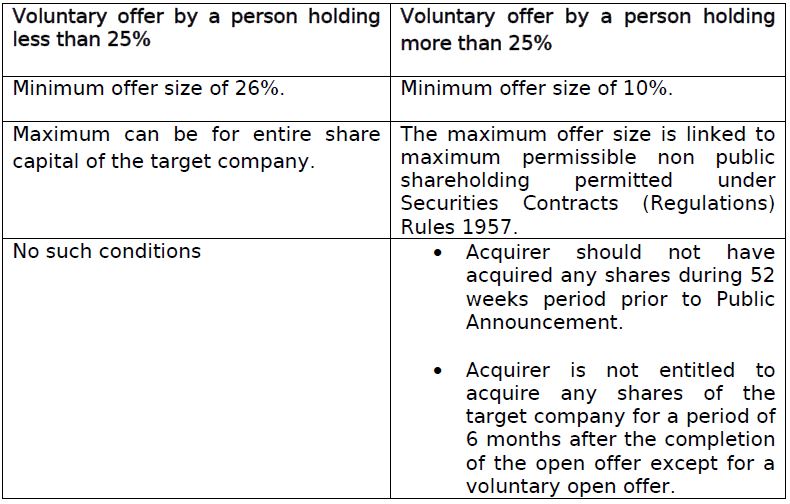

16. What is a voluntary open offer?

A voluntary open offer under Regulation 6, is an offer made by a person who himself or through Persons acting in concert ,if any, holds 25% or more shares or voting rights in the target company but less than the maximum permissible non-public shareholding limit.

17. What are the restrictions on acquirers making a voluntary open offer?

A voluntary offer cannot be made if the acquirer or PACs with him has acquired any shares of the target company in the 52 weeks prior to the voluntary offer. The acquirer is prohibited from acquiring any shares during the offer period other than those acquired in the open offer. The acquirer is also not entitled to acquire any shares for a period of 6 months, after completion of open offer except pursuant to another voluntary open offer.

18. Can a person holding less than 25% of the voting rights/ shares in a target company, make an offer?

Yes, any person holding less than 25% of shares/ voting rights in a target company can make an open offer provided the open offer is for a minimum of 26% of the share capital of the company.

19. How is the voluntary offer made by a person holding less than 25% of shares/ voting rights in a target company different from the voluntary offer made by a person holding more than 25% of shares/ voting rights of the target company?

20. Proposed acquisition of which type of securities, beyond the stipulated thresholds, leads to an obligation of making an open offer?

Acquisition of equity shares carrying voting rights or any security which entitles the holder thereof to exercise voting rights, beyond the prescribed threshold limits, leads to the obligation of making an open offer. GDR (Global Depository Receipts) which by virtue of depository agreement or otherwise, carrying voting rights is an example of a security which entitles the holder to exercise voting rights but is not an equity share.

21. Do all acquisitions of shares in excess of the prescribed limits and / or control lead to an open offer?

No. In respect of certain acquisitions, SAST Regulations, 2011 provide exemption from the requirements of making an open offer, subject to certain conditions being fulfilled. For example, acquisition pursuant to inter- se transfer of shares between certain categories of shareholders; acquisition in the ordinary course of business by entities like Underwriter registered with SEBI, stock brokers, merchant bankers acting as stabilizing agent, Scheduled Commercial Bank (SCB), acting as an escrow agent; etc. For more details, please refer to regulation 10 of SAST Regulations, 2011.

22. Does SEBI have the power to grant exemption to an acquirer from making an open offer or grant relaxation from the strict compliance with prescribed provisions of the open offer process, even if the proposed acquisition of shares or control is not covered under the exemptions prescribed in SAST Regulations,2011?

Yes. In the interest of the securities market, upon an application made by the acquirer, SEBI has the power to grant exemption from the requirements of making an open offer or grant a relaxation from strict compliance with prescribed provisions of the open offer process.

Before undertaking such acquisition, SEBI may at its discretion refer the application to a panel of experts constituted by SEBI. The orders passed in such matters would be uploaded on SEBI’s website.

23. Do only direct acquisitions of shares or control of the target company lead to the requirement of making an open offer?

No. The requirement to make an open offer arises even if there is an indirect acquisition of shares and / or control of the target company. An indirect acquisition would be the acquisition of shares or control over another entity by an acquirer that would enable the acquirer to exercise or direct to exercise voting rights beyond the stipulated thresholds or control over the target company.

24. What is a competitive offer?

Competitive offer is an offer made by a person, other than the acquirer who has made the first public announcement. A competitive offer shall be made within 15 working days of the date of the Detailed Public Statement (DPS) made by the acquirer who has made the first PA.

25. What happens if there is a competitive offer?

If there is a competitive offer, the acquirer who has made the original public announcement can revise the terms of his open offer provided the revised terms are favorable to the shareholders of the target company. Further, the bidders are entitled to make revision in the offer price up to 3 working days prior to the opening of the offer. The schedule of activities and the offer opening and closing of all competing offers shall be carried out with identical timelines.

26. What is a conditional offer?

An offer in which the acquirer has stipulated a minimum level of acceptance is known as a ‘conditional offer’.

27. What is meant by the term ‘minimum level of acceptance’?

‘Minimum level of acceptance’ implies minimum number of shares which the acquirer desires under the said conditional offer. If the number of shares validly tendered in the conditional offer, are less than the minimum level of acceptance stipulated by the acquirer, then the acquirer is not bound to accept any shares under the offer.

28. If the minimum level of acceptance is not reached, can the acquirer acquire shares under the Share Purchase Agreement, which triggered the offer?

In a conditional offer, if the minimum level of acceptance is not reached, the acquirer shall not acquire any shares in the target company under the open offer or the Share Purchase Agreement which has triggered the open offer.

29. What is the stipulated size of an open offer?

An open offer, other than a voluntary open offer under Regulation 6, must be made for a minimum of 26% of the target company’s share capital. The size of voluntary open offer under Regulation 6 must be for at least 10% of the target company’s share capital. Further the offer size percentage is calculated on the fully diluted share capital of the target company taking in to account potential increase in the number of outstanding shares as on 10th working day from the closure of the open offer.

30. What is ‘offer price’ and can the acquirer revise the offer price?

Offer price is the price at which the acquirer announces to acquire shares from the public shareholders under the open offer. The offer price shall not be less than the price as calculated under regulation 8 of the SAST Regulations, 2011 for frequently or infrequently traded shares.

Acquirer can make an upward revision to the offer price at any time up to 3 working days prior to the opening of the offer.

31. How do you determine whether the shares of the target company are frequently traded or infrequently traded?

The shares of the target company will be deemed to be frequently traded if the traded turnover on any stock exchange during the 12 calendar months preceding the calendar month, in which the PA is made, is at least 10% of the total number of shares of the target company. If the said turnover is less than 10%, it will be deemed to be infrequently traded.

32. How is the offer price calculated in case shares are frequently traded on the stock exchange?

If the target company’s shares are frequently traded then the open offer price for acquisition of shares under the minimum open offer shall be highest of the following:

- Highest negotiated price per share under the share purchase agreement (“SPA”) triggering the offer;

- Volume weighted average price of shares acquired by the acquirer during 52 weeks preceding the public announcement (“PA”);

- Highest price paid for any acquisition by the acquirer during 26 weeks immediately preceding the PA;

- Volume weighted average market price for sixty trading days preceding the PA.

- 33. How is the offer price calculated in case shares are infrequently traded on the stock exchange?

If the target company’s shares are infrequently traded then the open offer price for acquisition of shares under the minimum open offer shall be highest of the following: - Highest negotiated price per share under the share purchase agreement (“SPA”) triggering the offer;

- Volume weighted average price of shares acquired by the acquirer during 52 weeks preceding the public announcement (“PA”);

- Highest price paid for any acquisition by the acquirer during 26 weeks immediately preceding the PA;

- The price determined by the acquirer and the manager to the open offer after taking into account valuation parameters including book value, comparable trading multiples, and such other parameters that are customary for valuation of shares of such companies.

It may be noted that the Board may at the expense of the acquirer, require valuation of shares by an independent merchant banker other than the manager to the offer or any independent chartered accountant in practice having a minimum experience of 10 years.

34. Will the promoter be entitled to non-compete or any other fees other than the offer price?

As per the SAST Regulations, 2011, all shareholders will be given equitable treatment and no Promoter or shareholder can be paid any extra price, by whatever name it may be called.

35. Are there special provisions for determining the offer price in case of open offer arising out of indirect acquisition of a target company?

Yes. Since indirect acquisitions involve acquiring the target company as a part of a larger business, SAST Regulations, 2011 have prescribed additional parameters to be taken into account for determination of the offer price. If the size of the target company exceeds certain thresholds as compared to the size of the entity or business being acquired then the acquirer is required to compute and disclose in the letter of offer, the per share value of the target company taken into account for the acquisition, along with the methodology. (Kindly refer to Regulation 5). Further, in indirect acquisitions which are not in the nature of deemed direct acquisition, the offer price shall stand enhanced by an amount equal to a sum determined at the rate of 10% per annum for the period between the date on which primary acquisition was contracted and the date of Detailed Public Statement.

36. What is the difference between ‘offer period’ and ‘tendering period’?

The term ‘offer period’ pertains to the period starting from the date of the event triggering open offer till completion of payment of consideration to shareholders by the acquirer or withdrawal of the offer by the acquirer as the case may be.

The term ‘tendering period’ refers to the 10 working days period falling within the offer period, during which the eligible shareholders who wish to accept the open offer can tender their shares in the open offer.

37. Who are eligible shareholders?

All shareholders of the target company other than the acquirer, persons acting in concert with him and the parties to underlying agreement which triggered open offer including persons deemed to be acting in concert with such parties, irrespective of whether they are shareholders as on identified date or not.

38. What are the typical steps and corresponding timelines, in an open offer process?

Under most scenarios (except in certain types of indirect acquisitions) on the day of the triggering event, the acquirer is required to make a Public Announcement to the stock exchanges where shares of Target Company are listed and to SEBI. Within 5 working days thereafter, the acquirer is required to publish a Detailed Public Statement (DPS) in newspapers and also submit a copy to SEBI, after creation of an escrow account.

Within 5 working days of publication DPS, the acquirer through the manager to the offer is required to file a draft letter of offer with SEBI for its observations. The letter of offer is dispatched to the shareholders of the target company, as on the identified date, after duly incorporating the changes indicated by SEBI, if there are any.

The offer shall open not later than 12 working days from the date of receipt of SEBI’s observations. The acquirer is required to issue an advertisement announcing the final schedule of the open offer, one working day before opening of the offer. The offer shall remain open for 10 working days from the date of opening of the offer. Within 10 working days after the closure of the offer, the acquirer shall make payments to the shareholders whose shares have been accepted. A post offer advertisement, giving details of the acquisitions, is required to be published by the acquirer within 5 workings days of the completion of payments under the open offer.

39. What is ‘identified date’ in the context of SAST Regulations, 2011?

Identified date means the date 10 working days prior to the commencement of the tendering period, for the purposes of determining the shareholders of the target company to whom the letter of offer along with the form of acceptance shall be sent.

40. What is the purpose of the escrow account in the open offer process?

The acquirer is required to deposit some percentage of the offer price, in an escrow account before issuing a Detailed Public Statement. This serves as a security for performance of acquirer’s obligations under the open offer.

40A.Can cash component of the escrow account in the open offer process be maintained in an interest bearing account? (Inserted on 2-11-2015.)

Yes, the cash component of the escrow account may be maintained in an interest bearing account. However, the merchant banker shall ensure that the funds are available at the time of making payment to shareholders.

41. At what point of time in the process does a Merchant Banker need to be appointed and what is its role in the open offer process?

The Acquirer is required to appoint a Merchant Banker, registered with SEBI, as manager to the open offer before making the PA. The PA is required to be made through the said manager to the open offer.

The manager to the open offer has to exercise due diligence and ensure compliance with SAST Regulations, 2011. The manager to the open offer has to ensure that the contents of the PA, DPS, letter of offer and the post offer advertisement are true, fair and adequate in all material aspects and are in compliance with the requirements of SAST Regulations, 2011. Further, the manager to the open offer has to ensure that the acquirer is able to implement the open offer and firm arrangements for funds through verifiable means have been made by the acquirer to meet the payment obligations under the open offer.

42. What is a letter of offer? Does SEBI approve the draft Letter of Offer?

The letter of offer is a document which is dispatched to all shareholders of the target company as on identified date. This is also made available on the website of SEBI.

Prior to dispatch of letter of offer to shareholders, a draft letter of offer is submitted to SEBI for observations. SEBI may give its comments on the draft letter of offer as expeditiously as possible, but not later than 15 working days of the receipt of the draft letter of offer. SEBI may also seek clarifications and additional information from the manager to the offer and in such a case the period for issuance of comments shall be extended to the fifth working day from the date of receipt of satisfactory reply to the clarifications or additional information sought.

Filing of draft Letter of Offer with SEBI should not in any way be deemed or construed to mean that the same has been cleared, vetted or approved by SEBI. The draft Letter of Offer is submitted to SEBI for the limited purpose of overseeing whether the disclosures contained therein are generally adequate and are in conformity with the Regulations. SEBI does not take any responsibility either for the truthfulness or correctness of any statement, financial soundness of acquirer, or of PACs, or of the Target Company, whose shares are proposed to be acquired or for the correctness of the statements made or opinions expressed in the Letter of Offer.

43. How do I find the status of the draft letter of offer filed with SEBI?

SEBI updates the processing status of draft letter of offers filed with it on its website on a periodic basis under the section “offer documents”.

44. What are the disclosures required under the Public Announcement?

Public Announcement contains minimum details about the offer, the transaction that triggered the open offer obligations, acquirer, selling shareholders (if any), offer price and mode of payment. SEBI has prescribed format of Public Announcement, which is available in the SEBI website.

45. What are the disclosures required under the Detailed Public Statement?

Detailed Public Statement contains disclosure in more detail about the acquirer/PACs, target company, financials of the acquirers/PACs/target company, the offer, terms & conditions of the offer, procedure for acceptance and settlement of the offer, escrow account etc. SEBI has prescribed the format for Detailed Public Statement. The same is available in the SEBI website.

46. What are the disclosures required under the Letter of offer?

Letter of offer contains details about the offer, background of Acquirers/PACS, financial statements of Acquirer/ PACs, escrow arrangement, background of the target company, financial statements of the target company, justification for offer price, financial arrangements, terms and conditions of the offer, procedure for acceptance and settlement of the offer. SEBI has prescribed the format for Letter of offer, which enumerates minimum disclosure requirements. The Manager to the offer/ acquirer is free to add any other disclosures which in his opinion are material for the shareholders. The format is available in the SEBI website.

47. Is the financial disclosure standard as outlined in the Format for Detailed Public Statement (DPS) to the Shareholders of the Target Company (TC) in terms of Regulation 15(2)in point I(A) applicable to PACs too since the above clause refers just to the Acquirer ?

Yes, as clearly indicated in the format, the details of financial disclosure are required to be given for the acquirer as well Persons acting in concert with Acquirers.

48. If an acquirer enters into a SPA and triggers an open offer, when can the acquirer acquire shares proposed to be transferred under the SPA?

The acquirer can acquire shares under the SPA only after payment in respect of shares accepted under the open offer is complete but not later than 26 weeks from the expiry of the offer period.

49. What is the role of the target company in the open offer process?

Once a PA is made, the board of directors of the Target Company is expected to ensure that the business of the target company is conducted in the ordinary course. Alienation of material assets, material borrowings, issue of any authorized securities, announcement of a buy- back offer etc. is not permitted, unless authorized by shareholders by way of a special resolution by postal ballot.

The target company shall furnish to the acquirer within two working days from the identified date, a list of shareholders and a list of persons whose applications, if any, for registration of transfer of shares, in case of physical shares, are pending with the target company.

After closure of the open offer, the target company is required to provide assistance to the acquirer in verification of the shares tendered for acceptance under the open offer, in case of physical shares.

Upon receipt of the detailed public statement, the board of directors of the target company shall constitute a committee of independent directors to provide reasoned recommendations on such open offer, and the target company shall publish such recommendations and such committee shall be entitled to seek external professional advice at the expense of the target company. The recommendations of the Independent Directors are published in the same newspaper where the Detailed Public Statement is published by the acquirer and are published at least 2 working days before opening of the offer. The recommendation will also be sent to SEBI, Stock Exchanges and the Manager to the offer.

50. What is the manner in which the acquirer decides the acceptances from each shareholder?

The registrar to the open offer validates all the tenders in the open offer and creates a basis of acceptance in consultation with the manager to the open offer detailing validly and invalidly tendered shares received in the open offer.

In case, the valid shares tendered are less than the offer size, all the valid tendered shares are accepted. If the validly tendered shares in the open offer are more than the offer size, then the valid tenders are accepted on a proportionate basis. This is illustrated as below:

The company has a paid up share capital of Rs, 10,000/- (1000 shares of Rs. 10/- each) and shareholder A is holding 50 shares totaling to Rs. 500. In case an open offer is made for 26% of the share capital and the shares tendered are 300 which are in excess of the 26% shareholding, the shares will be accepted by the acquirer on a proportionate basis.

No of shares of A accepted = ((total no of shares offered X (no of shares

in the open offer) tendered by A ))

————————————

(Total shares tendered in the Open offer by all investors)

= 260 X 50 =43.33 shares~43 shares

—————-

300

Shares which are invalid or are rejected due to the valid acceptances being more than the offer size are subsequently returned to the respective shareholders within 10 working days of the closure of the open offer.

51. What are the modes of payment under the open offer?

Payment considerations by the acquirer under the open offer can be made by cash and / or by issue of equity shares and / or secured debt instruments (investment grade) and / or convertible debt instruments (convertible to equity shares) of acquirer (or PACs, if any) if such equity shares and secured debt instruments are listed.

The chosen mode of payment is required to be disclosed in the open offer document meant for shareholders of the target company.

52. Can an acquirer withdraw the open offer once made?

An open offer once made cannot be withdrawn except in the following circumstances:

Statutory approvals required for the open offer or for effecting the acquisitions attracting the obligation to make an open offer have been refused subject to such requirement for approvals having been specifically disclosed in the DPS and the letter of offer;

Any condition stipulated in the SPA attracting the obligation to make the open offer is not met for reasons outside the reasonable control of the acquirer, subject to such conditions having been specifically disclosed in the DPS and the letter of offer;

Sole acquirer being a natural person has died;

Such circumstances which in the opinion of SEBI merit withdrawal of open offer.

53. If post open offer the shareholding of the acquirer goes beyond the maximum permissible non public shareholding limit, can the acquirer immediately make a delisting offer in terms of Delisting Regulations. ?

No. The acquirer cannot launch a voluntary delisting offer in terms of Delisting Regulations of SEBI, unless a period of twelve months has elapsed from the date of the completion of the offer period.

54. I was not holding shares on the identified date but acquired shares subsequently. Am I eligible to participate in the open offer?

Yes. Shareholders who acquire shares after the identified date are eligible to participate in the open offer provided they submit their valid tenders before the end of the tendering period.

You may send a request to the registrar to the open offer or manager to the open offer for obtaining the letter of offer including the form of acceptance. Alternately, you can make an application on plain paper giving certain specific details. Please refer to the Detailed Public Statement of the acquirer for instructions in this regard.

55. How will shareholder of the target company know that an open offer is made by the acquirer?

SAST Regulations, 2011 provides for wide dissemination of the information related to an open offer. The DPS and pre-offer announcements before commencement of the tendering period are published in national newspapers as well as in one newspaper of the regional language of the place where registered office of the target company is located.

The final letter of offer is required to be dispatched to all shareholders whose names appear as shareholders as on the identified date. Further, the PA, the DPS and other announcements are also filed with the stock exchange and SEBI, and are uploaded on their respective websites for information dissemination.

56. For how many days is an open offer required to be kept open?

The offer is required to be kept open for ten working days.

57. How do I get the Letter of Offer and tender my shares under the open offer?

The letter of offer along with form of acceptance is sent to all eligible shareholders of the target company, who are shareholders of the target company as on the identified date. The eligible shareholder has to fill in the form of acceptance sent along the letter of offer and submit the same to the registrar to the open offer or the manager to the open offer. In case the shareholder has not received the letter of offer, such shareholder can request the registrar to the open offer or manager to the open offer for the same. Further, the letter of offer along with the form of acceptance will also be available on SEBI’s website.

58. What are the documents that the shareholders should go through before tendering their shares pursuant to the open offer?

Before tendering their shares pursuant to the open offer, the shareholders are advised to go through the Detailed Public Statement, Letter of offer and also the recommendations and observations of the Committee of Independent Directors on the offer. It may be noted that all the aforesaid documents are available on SEBI website. Further the recommendations of the Independent Directors are published in the same newspaper where the Detailed Public Statement is published by the acquirer and are published at least 2 working days before opening of the offer.

59. Do I need to convert my physical shares into demat before tendering in the open offer?

Shareholders need not convert their physical shares into demat form before tendering shares in the open offer. Physical shares can be tendered in an open offer along with the form of acceptance and such documents as mentioned in the section ‘Procedure for acceptance and settlement of the Offer’ in the letter of offer.

60. Can I withdraw or revise my tender?

No. Once a shareholder has tendered his shares in the open offer made by the acquirer, he/ she cannot withdraw/ revise his/her request.

61. Can I tender my shares after the closure of the tendering period?

No. Your acceptance for tendering shares in the offer should reach the collection center on or before the last date of tendering period.

62. I hold shares which are partly paid-up. Can I tender these shares in the open offer?

Yes, partly paid-up shares can be tendered in the open offer. The letter of offer contains the offer price of the partly paid up share, which can be different from the offer price for fully paid up share.

63. When will the shareholder receive (i) intimation about acceptance/ rejection of his shares tendered under the open offer or (ii) consideration for shares accepted by the acquirer?

The shareholder shall receive (i) intimation about acceptance/ rejection of his shares tendered under the open offer or (ii) consideration for shares accepted by the acquirer, within 10 working days of the closure of the open offer.

64. What happens if regulatory approvals are delayed?

If the regulatory approvals required for completing the open offer and acquisition are delayed, the acquirer may be unable to make the payment within 10 working days of closure of open offer. In such an event, SEBI may grant extension of time for making payments, subject to the acquirer agreeing to pay interest to the shareholders of the target company for the delay at such rate as may be specified by SEBI.

If statutory approvals are required for some but not all shareholders, the acquirer can make payment to such shareholders in respect of whom no statutory approvals are required in order to complete the open offer.

65. If the payment is delayed beyond 10 working days of the closure of the tendering period (closure of open offer), will the acquirer be required to compensate the public shareholders who have participated under the offer?

Acquirer is required to complete the payment of consideration to shareholders who have accepted the offer within 10 working days from the date of closure of the open offer. If there is a delay in payment of consideration (not due to non-receipt of statutory approvals), it would be treated as a violation of the SAST Regulations, 2011 and SEBI may issue direction to such acquirer including direction to pay interest.

66. Whom do I approach if I have any grievance in respect of the open offer, delay in receipt of consideration / unaccepted shares etc.?

The shareholder of the target company should approach the manager to the open offer or the registrar to the open offer for any grievance. However, if the shareholder is not satisfied or does not receive a satisfactory response to his / her grievance, he may approach SEBI through online SEBI Complaint Redressal System (SCORES) at www.scores.gov.in.

In case, during the open offer or before the starting of the open offer, any investor has any comment/ complaint about the disclosures given by the acquirer in Public Announcement or in Detailed Public statement or in draft Letter of offer information, he can write to Corporate Finance Department, Division of Corporate Restructuring at SEBI Bhavan, Plot No.C4-A, ‘G’ Block, Bandra Kurla Complex, Bandra (E), Mumbai 400 051. Please note that PA/DPS, Draft Letter of offer are also available on website of SEBI.

67. Where can an investor get more information related to the SAST Regulations, 2011?

An investor can get more information related to the SAST Regulations, 2011 from the SEBI website and from the Investors website of SEBI.

68. What are the disclosures (other than the ones given in PA/ DPS/ Letter of offer for the open offer) required to be made in terms of SAST Regulations, 2011, by whom, when and to whom?

Event based Disclosures

(Please note the word “shares” for disclosure purposes include convertible securities also.)

a. Any person, who along with PACs crosses the threshold limit of 5% of shares or voting rights, has to disclose his aggregate shareholding and voting rights to the Target Company at its registered office and to every Stock Exchange where the shares of the Target Company are listed within 2 working days of acquisition as per the format specified by SEBI.

b. Any person who holds 5% or more of shares or Voting rights of the target company and who acquires or sells shares representing 2% or more of the voting rights, shall disclose details of such acquisitions/ sales to the Target company at its registered office and to every Stock Exchanges where the shares of the Target Company are listed within 2 working days of such transaction, as per the format specified by SEBI.

Continual disclosures of aggregate shareholding shall be made within 7 days of financial year ending on March 31 to the target company at its registered office and every stock exchange where the shares of the Target Company are listed by:

a. Shareholders (along with PACs, if any) holding shares or voting rights entitling them to exercise 25% or more of the voting rights in the target company.

b. Promoter (along with PACs, if any) of the target company irrespective of their percentage of holding.

Disclosures of encumbered shares

a. The promoter (along with PACs) of the target company shall disclose details of shares encumbered by them or any invocation or release of encumbrance of shares held by them to the target company at its registered office and every stock exchange where shares of the target company are listed, within 7 working days of such event.

69. How to compute trigger limits specified above for disclosures.

The word “shares” for disclosure purposes include convertible securities also. Hence for computation of trigger limits for disclosures given above, percentage w.r.t shares shall be computed taking in to account total number of equity shares and convertibles and the percentage w.r.t voting rights shall be computed after considering voting rights on equity shares and other securities (like GDRs, if such GDRs carry voting rights)

An illustration is provided below for the calculation of trigger limits for disclosures given in point (b) of the reply to query (13).

Total Shares/ voting capital of the company

Company A has 100 equity shares, 50 partly convertible Debentures (PCDs) and 10 GDRs. 1 GDR carries 1 voting right.

Total shares of company A= 100+50+10 = 160

Total voting capital of Company A= 100+10=110

Persons B’s holding of shares and voting rights

Person B has 8 equity shares, 7 PCDs and 1 GDR.

Person B has 8+7+1 =16 shares (shares for disclosure purpose includes convertible securities)

Person B’s holding in terms of shares= 16/160=10% of shares

Person B’s voting rights= 8+1= 9 voting rights

Person B’s holding in terms of voting rights = 9/110=8 % of voting rights

Since person B is holding more than 5% of shares or voting rights, he is required to make disclosures for any acquisition/ sale of 2% or more of shares or voting rights.

Acquisition by Person B

Scenario I

Person B acquires 2 equity shares and 2 PCDs.

In terms of shares, person B has acquired 4/160=2.5% of shares

In terms of voting rights, person B has acquired 2/110= 1.8% of voting rights

Since acquisition done by person B represents 2 % or more of shares, the disclosure obligation as stated at Reply of Q-13(b) is triggered.

Scenario II

Person B acquires 20 PCDs

In terms of shares, person B has acquired 20 shares, i.e. 20/160 i.e. 12.5% shares.

In terms of voting rights, he has not acquired a single voting right i.e. 0 voting right

However, since acquisition done by person B represents 2% or more of shares (though no voting rights), the disclosure obligations as stated at (b) in reply 13 is triggered.

70. Whether promoters are required to disclose details of arrangements which place encumbrances on shares like lock-in stipulations, non- disposal undertaking, right of first refusal etc?

As per Regulation 28(3), the term “encumbrance” shall include a pledge, lien or any such transaction, by whatever name called.” The promoters have to understand the nature of encumbrance and those encumbrances which entail a risk of the shares held by promoters being appropriated or sold by a third party, directly or indirectly, are required to be disclosed to the stock exchanges in terms of the Takeover Regulations, 2011.

71. If the shares of the holding company of a target company are pledged, whether the same would be covered under disclosures of “Encumbered shares” by promoters of the Target Company?

Yes, details of such pledge would be covered under disclosure of “encumbrance” as required under the Regulations

72. Whether furnishing of a Non Disposal Undertaking (NDU) by promoters to the lenders would be covered under disclosures of “Encumbered shares” by promoters of the Target Company?

Yes, all types of NDUs by promoters will be covered under the scope of disclosures of “Encumbrances” under the Regulations. These NDUs may, inter-alia, include undertaking for:

(i) not encumbering shares to another party without the prior approval of the party with whom the shares have been encumbered;

(ii) non-disposal of shares beyond a certain threshold so as to retain control;

(iii) Non-disposal of shares entailing risk of appropriation or invocation by the party with whom the shares have been encumbered or for its benefit.(Note)

(Note :Substituted for “No, mere NDU by promoters will not be covered under the scope of disclosures of Encumbrance under the Regulations. However if NDUs are given along with side-agreements which may entail the risk of shares held by the promoters being appropriated or sold by a third party, directly or indirectly, the same needs to be disclosed.”)

73. What happens if the Acquirer / Target Company / Merchant Banker or the Manager to the open offer violates the provisions of the SAST Regulations, 2011?

SAST Regulations, 2011 have laid down the general obligations of acquirer, Target Company and the manager to the open offer. For failure to carry out these obligations as well as for failure / non-compliance of other provisions of these Regulations, penalties have been laid down there under. These penalties include:

directing the divestment of shares acquired;

directing the transfer of the shares / proceeds of a directed sale of shares to the investor protection fund;

directing the target company / any depository not to give effect to any transfer of shares;

directing the acquirer not to exercise any voting or other rights attached to shares acquired;

debarring person(s) from accessing the capital market or dealing in securities;

directing the acquirer to make an open offer at an offer price determined by SEBI in accordance with the Regulations;

directing the acquirer not to cause, and the target company not to effect, any disposal of assets of the target company or any of its subsidiaries unless mentioned in the letter of offer;

directing the acquirer to make an offer and pay interest on the offer price for having failed to make an offer or has delayed an open offer;

directing the acquirer not to make an open offer or enter into a transaction that would trigger an open offer, if the acquirer has failed to make payment of the open offer consideration;

directing the acquirer to pay interest of for delayed payment of the open offer consideration;

directing any person to cease and desist from exercising control acquired over any target company;

directing divestiture of such number of shares as would result in the shareholding of an acquirer and persons acting in concert with him being limited to the maximum permissible non-public shareholding limit or below.

74. What is the procedure for a company or an intermediary in case it needs clarification or an interpretation of some provisions of SAST Regulations, 2011?

SEBI updates its FAQs section based on the queries received. You are advised to see the FAQs section. However for seeking interpretation of a particular provision or a no action letter pertaining to a particular transaction, the applicant is advised to apply under the provisions of SEBI (informal Guidance) Scheme, 2003, details of which are available on the SEBI website.