[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

[CENTRAL BOARD OF DIRECT TAXES]

Income-tax

Notification No. 54/2016

New Delhi, the Dated: 27th June, 2016

S.O.2213(E).─ In exercise of the powers conferred by clause(ha) of sub-section (2) of section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax (18th Amendment) Rules, 2016.

(2) They shall come into force on the 1st day of April, 2017.

2. In the Income-tax Rules, 1962 (hereinafter referred to as the said rules), after rule 127, following rule shall be inserted, namely:-

“128. Foreign Tax Credit.– (1) An assessee, being a resident shall be allowed a credit for the amount of any foreign tax paid by him in a country or specified territory outside India, by way of deduction or otherwise, in the year in which the income corresponding to such tax has been offered to tax or assessed to tax in India, in the manner and to the extent as specified in this rule:

Provided that in a case where income on which foreign tax has been paid or deducted, is offered to tax in more than one year, credit of foreign tax shall be allowed across those years in the same proportion in which the income is offered to tax or assessed to tax in India.

(2) The foreign tax referred to in sub-rule (1) shall mean,-

(a) in respect of a country or specified territory outside India with which India has entered into an agreement for the relief or avoidance of double taxation of income in terms of section 90 or section 90A, the tax covered under the said agreement;

(b) in respect of any other country or specified territory outside India, the tax payable under the law in force in that country or specified territory in the nature of income-tax referred to in clause (iv) of the Explanation to section 91.

(3) The credit under sub-rule (1) shall be available against the amount of tax, surcharge and cess payable under the Act but not in respect of any sum payable by way of interest, fee or penalty.

(4) No credit under sub-rule (1) shall be available in respect of any amount of foreign tax or part thereof which is disputed in any manner by the assessee:

Provided that the credit of such disputed tax shall be allowed for the year in which such income is offered to tax or assessed to tax in India if the assessee within six months from the end of the month in which the dispute is finally settled, furnishes evidence of settlement of dispute and an evidence to the effect that the liability for payment of such foreign tax has been discharged by him and furnishes an undertaking that no refund in respect of such amount has directly or indirectly been claimed or shall be claimed.

(5) The credit of foreign tax shall be the aggregate of the amounts of credit computed separately for each source of income arising from a particular country or specified territory outside India and shall be given effect to in the following manner:-

(i) the credit shall be the lower of the tax payable under the Act on such income and the foreign tax paid on such income:

Provided that where the foreign tax paid exceeds the amount of tax payable in accordance with the provisions of the agreement for relief or avoidance of double taxation, such excess shall be ignored for the purposes of this clause;

(ii) the credit shall be determined by conversion of the currency of payment of foreign tax at the telegraphic transfer buying rate on the last day of the month immediately preceding the month in which such tax has been paid or deducted.

(6) In a case where any tax is payable under the provisions of section 115JB or section 115JC, the credit of foreign tax shall be allowed against such tax in the same manner as is allowable against any tax payable under the provisions of the Act other than the provisions of the said sections (hereafter referred to as the “normal provisions”).

(7) Where the amount of foreign tax credit available against the tax payable under the provisions of section 115JB or section 115JC exceeds the amount of tax credit available against the normal provisions, then while computing the amount of credit under section 115JAA or section 115JD in respect of the taxes paid under section 115JB or section 115JC, as the case may be, such excess shall be ignored.

(8) Credit of any foreign tax shall be allowed on furnishing the following documents by the assessee, namely:-

(i) a statement of income from the country or specified territory outside India offered for tax for the previous year and of foreign tax deducted or paid on such income in Form No.67 and verified in the manner specified therein;

(ii) certificate or statement specifying the nature of income and the amount of tax deducted therefrom or paid by the assessee,-

(a) from the tax authority of the country or specified territory outside India; or

(b) from the person responsible for deduction of such tax; or

(c) signed by the assessee:

Provided that the statement furnished by the assessee in clause (c) shall be valid if it is accompanied by,-

(A) an acknowledgment of online payment or bank counter foil or challan for payment of tax where the payment has been made by the assessee;

(B) proof of deduction where the tax has been deducted.

(9) The statement in Form No.67 referred to in clause (i) of sub-rule (8) and the certificate or the statement referred to in clause (ii) of sub-rule (8) shall be furnished on or before the due date specified for furnishing the return of income under sub-section (1) of section 139, in the manner specified for furnishing such return of income.

(10) Form No. 67 shall also be furnished in a case where the carry backward of loss of the current year results in refund of foreign tax for which credit has been claimed in any earlier previous year or years.”.

Explanation.- For the purposes of this rule ‘telegraphic transfer buying rate’ shall have the same meaning as assigned to it in Explanation to rule 26.

3. In the said rules, in Appendix-II, after Form No.66, the following Form shall be inserted, namely:-

“FORM NO. 67

[See rule 128]

Statement of income from a country or specified territory outside India and Foreign Tax Credit

Part-A

1. Name of the assessee ______________________________________________________ 2. PAN

3. Address ______________________________________________________

4. Assessment year _______________________________________________

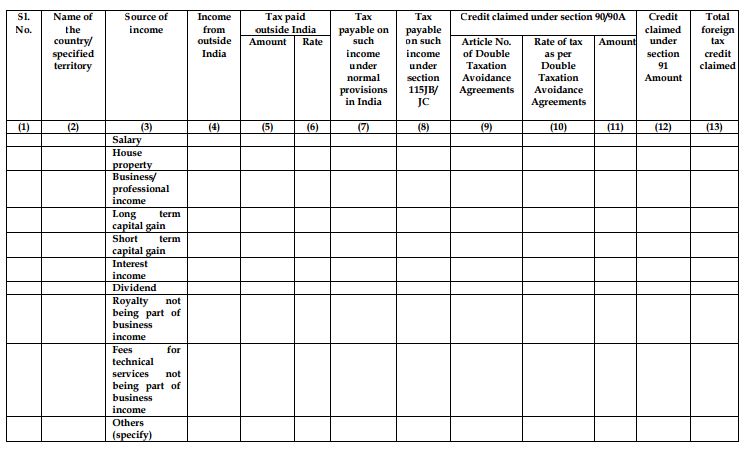

5. Details of income from a country or specified territory outside India and Foreign Tax Credit claimed

Part-B

1. (a) Whether any refund of foreign tax has been claimed in any Yes/ No

prior accounting year as a result of carry backward of losses

(b) If reply to (a) above is Yes, furnish the following details:-

(i) the accounting year to which such loss pertains _________

(ii) the accounting year(s) in which set off of carry backward _________

of loss has been undertaken

(iii) refund claimed for the accounting year(s) _________

(iv) previous year to which refund referred to in (iii) relates _________

2. (a) Whether credit for any foreign tax has been claimed which is under dispute Yes/ No

(b) If reply to (a) above is Yes, furnish the following details:-

(i) the nature and amount of income in respect of which tax is disputed _________

(ii) the amount of such disputed tax ________

Verification

I________________ son/daughter of ____________________, holding permanent account number _______________________ solemnly declare that to the best of my knowledge and belief, the information given in Part-A and Part-B of the statement above is correct and complete and is truly stated.

I further declare that I am making this statement in my capacity as ___________ and I am also competent to make this statement and verify it.

Verified today the __________day of ___________20___.

Place:______________

(Signature)

Note: Attach certificate or statement and proof of payment/deduction of foreign tax as referred to in clause (ii) of sub-rule (8) of rule 128.”.

[F.No. 142/24/2015 -TPL]

(Dr. T.S. Mapwal)

Under Secretary to the Government of India

Note.– The principal rules were published in the Gazette of India, Extraordinary, Part-II, Section 3, Sub-section (ii) vide notification number S.O.969(E), dated the 26th March, 1962 and last amended by vide notification number S.O. 2196 (E) dated 24/06/2016.