Ministry of Finance

Department of Economic Affairs

(Capital Market Division)

Frequently Asked Questions on

Rajiv Gandhi Equity Savings Scheme (RGESS)

5 February 2014

No. 1/8/SM/2012

Contents

I. Objectives and legal aspects of RGESS

- What is RGESS ?

- What is the objective of the Scheme ?

- What is the legal provision for RGESS?

- Would first time investors not lose money in the equity market? Would it be too dangerous for them to invest in it?

- We already have an Equity Linked Savings Scheme (ELSS)? Why do we need RGESS?

- What are the benefits / highlights of RGESS compared to other tax saving schemes?

II. Coverage of the Scheme: Investors and Investments allowed under RGESS

- Who all will be covered under the Scheme? Who is a new investor?

- I am a non-resident Indian; Am I eligible for RGESS?

- Can a Guardian claim RGESS tax benefit if investment is done in the name of Minor?

- I am already having physical units of mutual fund and / or Exchange Traded Funds; Am I eligible for the RGESS?

- I possess some physical shares; Am I eligible under RGESS?

- I possess some shares in the demat account; but they are of unlisted companies. Am I eligible?

- I have shares in demat account under the ESOP category? Am I eligible for tax benefit in RGESS?

- What are the investment options available under the Scheme? What are the “eligible securities” under RGESS?

- Where can I get information about these eligible stocks?

- Why RGESS Investments are limited to top 100 stocks?

- When I made the investment, the particular stock was in BSE 100; thereafter it was removed from the BSE 100 list by the exchange; Is my investment still eligible for RGESS when I file my returns?

- When I enrolled for RGESS my annual income was below Rs. 12 lakh. However, in the subsequent year it crossed Rs. 12 lakh. Am I eligible to claim benefits?

- I applied for the IPO / New Fund offer (NFO) in the month of March; However, the company / Scheme got listed in the stock exchange only in April i.e, in the next financial year. Is my investment eligible?

- For how many years I can avail of RGESS benefits?

- When does counting of my three year starts? What is “initial year”?

- Do I have to make my first investment, after designating my account, only in eligible scrip?

- Am I mandated to make investments in all three years?

- How much tax deduction will I be eligible under RGESS?

- What is the amount of deduction I am eligible for in a single financial year?

- I have invested less than Rs. 50,000 in a year. Can I invest more than Rs. 50,000 in subsequent years so that my total investments for three years are less than Rs. 1.5 lakhs?

- What is the maximum amount that I can invest in securities market? Can I bring the same in installments?

- I have already claimed tax benefit under Section 80C. Can I avail of RGESS?

- I want to invest more than Rs.50,000; how will I allocate my investments to the tune of Rs. 50 000 and claim benefit under RGESS?

- I have purchased shares of Company ‘A’ which is an eligible security under RGESS for Rs. 70,000; How can I free the shares of the same company beyond Rs. 50,000/-?

- When should I submit Form B or general application? Is there a time limit?

- Can I claim tax deduction in respect of the amount invested in eligible securities which are specified in Form B? 15

III. Investments through Mutual funds

- What are the types of mutual funds which would be eligible for investments under RGESS?

- What are closed-end mutual fund schemes?

- How frequently is the portfolio of RGESS mutual fund scheme published?

- What is Net Asset Value (NAV) of a scheme?

- How will investors determine the value of their units in RGESS mutual fund scheme?

- What are ETFs?

- How to subscribe to RGESS Mutual Fund schemes?

- Are RGESS mutual fund Schemes available for investment to regular investors who are not eligible for RGESS or who do not intend to avail of tax benefits under RGESS?

- Is a demat account compulsory for investing in RGESS mutual fund ?

- What documents / information do I need to submit with my RGESS mutual fund application form at the time of subscription during the NFO?

- What are the Plans offered by mutual fund schemes?

- What are the Options available under each of the above Plans?

- What is the frequency of dividends that will be declared in RGESS MF scheme?

- Do mutual fund schemes pay income tax?

- Are dividends distributed by mutual fund schemes taxed in the hands of investors?

- Where can I find the list of RGESS mutual fund schemes?

- Where should I submit my RGESS mutual fund application form during the NFO?

- When will the allotment be done for RGESS mutual fund?

- How will I be intimated about the allotment?

- When would the refund be done for rejected applications?

- Is there an option to exit from RGESS mutual fund before 3 years?

- What happens if investors do not trade and hold the units in a closed-ended mutual fund scheme till the maturity of the scheme?

- Is Systematic Investment Plan (SIP) available in RGESS?

- Can an investor switch existing Mutual Fund units to RGESS Scheme? Will I be eligible for tax benefits?

- What is the expense ratio charged under RGESS Mutual Fund scheme?

- What will be the entry / exit load charged to investors, if invested in RGESS Mutual Fund schemes?

- Whom can the investor contact for any complaint regarding RGESS Mutual Fund units?

IV Participating in the Scheme: Procedural and Operational issues.

- How to make RGESS eligible investments?

- I opened/activated the demat account for the purpose of availing of RGESS benefits. However, I forgot to submit Form A and started transacting through my account. Will I be considered ineligible for claiming benefits?

- Mr. A has a demat account and he does an off market transfer of eligible stocks into Mr.B’s account, who is a 1st time retail investor but still has not designated his account for RGESS. Is Mr. B eligible for RGESS?

- Is credit received in my demat account through dematerialisation eligible for claiming benefits under RGESS?

- What will be the mode of holding eligible securities?

- Should I need to get my mutual fund / ETF units also in demat form?

- I have purchased RGESS eligible mutual fund units in physical mode; Will I be eligible for tax benefit if I convert it to demat at a later date?

- Is there any need for the investor to open a dedicated demat account for availing of RGESS benefits? Can I hold other securities i.e., other than eligible securities in my demat account designated for RGESS?

- How to open RGESS demat account with a Depository Participant (DP)?

- How to open a trading account?

- What are the documents I need to bring for opening a demat / trading account?

- I belong to PAN exempt category (resident of Sikkim); Can I open an RGESS account without PAN?

- Should I ask for internet access to my trading and demat accounts?

- Can I designate an existing demat account under RGESS?

- Where will I get ‘Form A’ Form “B” etc?

- Can I designate or open more than one demat account for RGESS?

- Is there a low cost demat account for RGESS?

- What are the do’s and don’ts while operating in securities market?

- How can I register my complaints with respect to my transactions in securities market?

- If the RGESS account holder has expired and if the securities are under fixed lock-in, can it be transferred to the nominee / legal heir?

V. Implementation of Lock-in conditions and Valuation of securities under RGESS

- What will be the basis for valuation of initial investment made under RGESS for availing tax benefit?

- What is the holding period for investments made under RGESS?

- What is ‘Fixed Lock-in’ period? Has the concept changed from that adopted during FY 2012-13?

- I started my RGESS investment in FY 2012-13; Am I also bound by the new definition of fixed lock-in?

- When the lock-in period does start? From the date of purchase or from date of credit of securities in the demat account?

- Won’t the above method of calculating fixed lock in result in lock-in for more than three years?

- Can I sell / pledge eligible securities declared for RGESS during ‘Fixed Lock-in’ period?

- What is ‘Flexible Lock-in’ period?

- Can I trade / sell during flexible lock-in period?

- How the valuation of securities is done during the flexible lock-in period?

- How does DPs allot the fresh investments made in subsequent years?

- After first year, if the value of the RGESS eligible portfolio crosses the first year’s investment value can the excess value be considered as the new investment done in the second year?

- Is there a difference in the valuation of RGESS eligible securities as compared to the general valuation principle adopted by Depositories?

- How the three year lock-in condition is implemented?

- What will happen if I do not trade (sell/buy) eligible securities during ‘Flexible Lock-in’ period?

- What will happen to my demat account at the end of flexible lock-in period?

VI Monitoring and Penalties

- Do I have to value RGESS eligible securities for the purposes of compliance with the provisions of the Scheme?

- How do I claim for tax deduction?

- Who will give me new retail investor certificate and annual account statement?

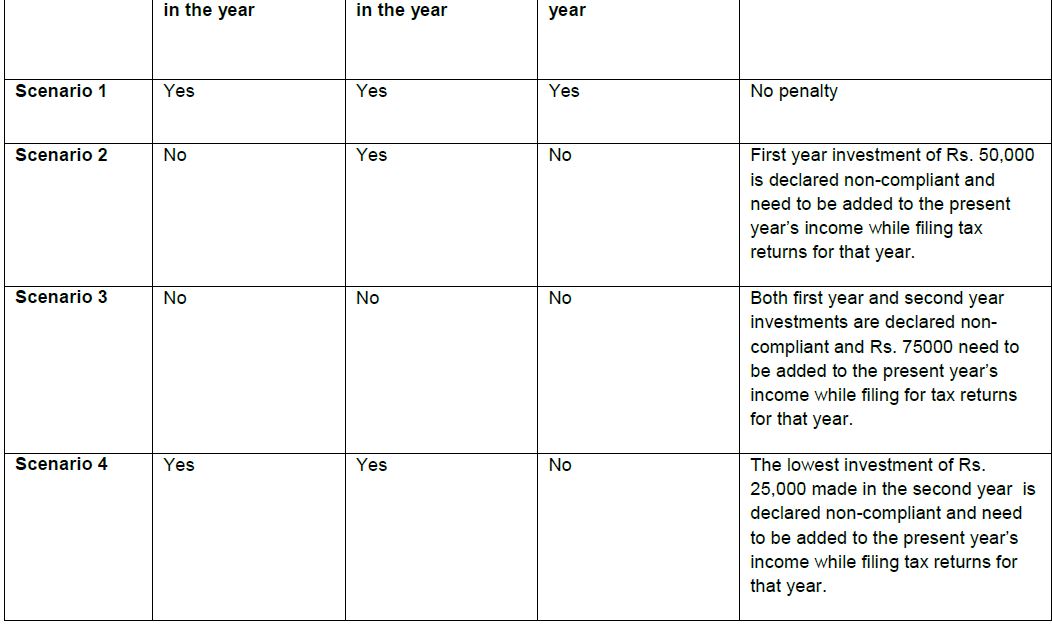

- What is the penalty if I violate the conditions of RGESS?

- How the penalty is calculated / allotted in case of investments for more than one year are in the flexible lock-in period?

- What will be the effect of different types of corporate actions like split, consolidation, bonus, rights, etc. on RGESS eligible investment during flexible lock in period?

- Does this FAQ replaces the FAQ released in FY 2012-13?

- How the Scheme is monitored?

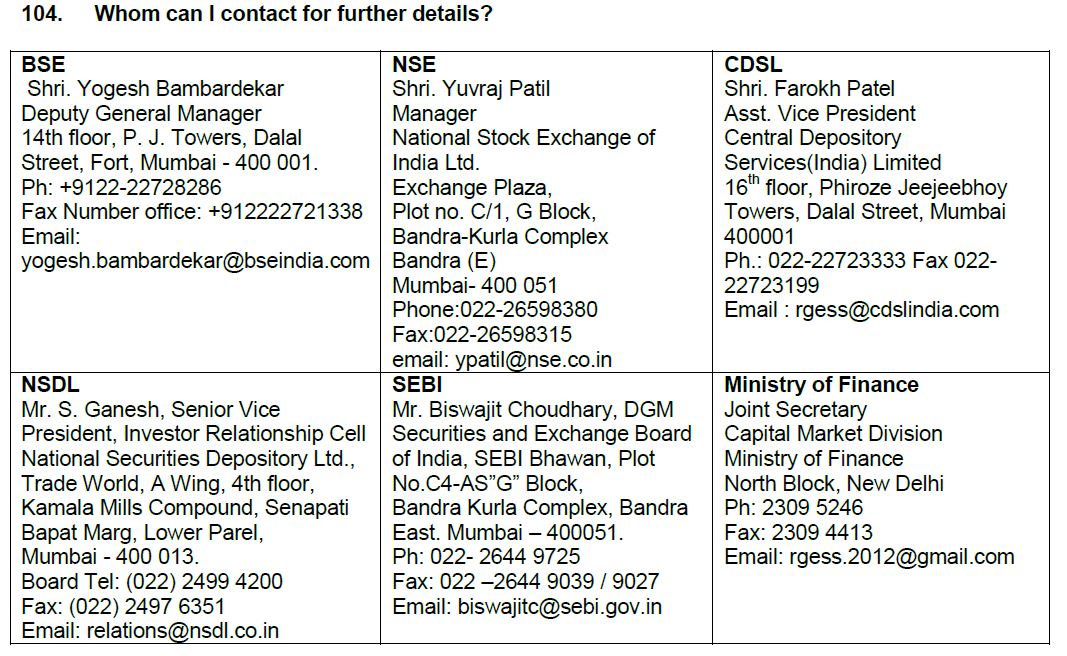

- Whom can I contact for further details?

I. Objectives and legal aspects of RGES

- What is RGESS

Rajiv Gandhi Equity Savings Scheme (RGESS), is a tax saving scheme announced in the Union Budget 2012-13 (para 35) and further expanded vide Union Budget 2013-14 (para 61 & 144). The scheme is designed exclusively for the first time individual investors in securities market, whose gross total income for the year is below a certain limit. In 2013-14, the income ceiling of the beneficiaries was raised to Rs. 12 lakh from Rs. 10 lakh specified in 2012-13. The investor would get under Section 80CCG of the Income Tax Act, a 50% deduction of the amount invested during the year, upto a maximum investment of Rs. 50,000 per financial year, from his/her taxable income for that year, for three consecutive assessment years.

- What is the objective of the Scheme?

As announced in the Union Budget 2012-13, the objective of the Scheme is to encourage the flow of savings and to improve the depth of domestic capital markets. This would help in promoting an ‘equity culture’ in India. The Scheme aims at widening the retail investor base in the Indian securities markets and also furthers the goal of financial stability and financial inclusion.

- What is the legal provision for RGESS?

A new section 80CCG in the Income tax Act, 1961 on ‘Deduction in respect of investment under an equity savings scheme’ was introduced vide Finance Act, 2012 and amended vide Finance Act, 2013, to give tax benefits to ‘New Retail Investors’ whose gross annual income is less than or equal to Rs.12 Lakhs, for investments in ‘Eligible Securities’ up to Rs.50,000 in a single financial year, for three consecutive assessment years.

The details of the RGESS Scheme were first notified on 23 November 2012 (Section No. 2777(E); Notification No. 51) and vide subsequent corrigendum dated 5 December 2012 (Section No. 2835(E); Notification No. 53) by Department of Revenue. The operational guidelines were issued by SEBI on 6 December 2012. Subsequent to the Union Budget 2013-14, Section 80CCG was amended vide Finance Act, 2013, to expand the scope of the Scheme. The notification dated 23 November, 2012 was accordingly amended vide Notification dated 18 December 2013 (Section No. 3693 (E); Notification No.94).

- Would first time investors not lose money in the equity market? Would it be too dangerous for them to invest in it?

The investors in the RGESS run the risk of losing money in the equity market, like any other investor in the securities market. The Scheme does not provide any guarantee of assured returns. Therefore, investors under RGESS are advised to do due diligence before making any investments in the equity market.

However, while designing the Scheme, safeguards like, restricting the investments to select large cap stocks, lock-in period with enough flexibility to take benefits of the positive market movements etc. have been provided to protect the interests of the first time investors.

To give the benefit of diversification and consequent risk minimization, investments into Exchange Traded Funds (ETFs) or Mutual funds, set up as per the criteria laid down in the Scheme, are also allowed under the Scheme.

- We already have an Equity Linked Savings Scheme (ELSS)? Why do we need RGESS?

ELSS and RGESS are entirely different schemes: They pertain to different asset classes with ELSS offering passive investment avenues. ELSS is meant for indirect participation in the stock market, whereas RGESS aims at encouraging direct participation in the stock market. The operational differences are given below:

| Operational differences | |

| ELSS | RGESS |

| Investments are to be strictly in mutual funds | Investments are to be made directly in listed equity or into units of mutual funds and ETFs |

| 100% deduction (upto Rs. 1,00,000) is allowed under ELSS | Only 50% deduction of the investment made (upto max. of Rs. 25,000 in any one year) is allowed under RGESS. |

| ELSS benefits can be availed by an investor every year | RGESS benefits are limited to the new investors and can be availed for only 3 consecutive years |

| The ELSS benefit is coming under Section 80C of the IT Act which has an aggregate limit of Rs. 1,00,000 for all such eligible instruments like LIC policy, PPF etc | RGESS deduction is available under Section 80CCG. This is a separate investment limit exclusively for RGESS, over and above the Section 80C Limit of Rs. 1 lakh |

| Lock-in period of 3 years | Lock-in period of 3-years. However, trading allowed after one-year, subject to conditions. |

| Since investments are in mutual funds, it is perceived to be less risky | Since investments are in equity, risk is perceived to be higher |

- What are the benefits / highlights of RGESS compared to other tax saving schemes?

The following are the benefits of RGESS:

- The allowed tax deduction u/s 80CCG will be over and above the Rs. 1 Lakh limit permitted under Section 80C of the Income Tax (IT) Act, making it thus attractive for the middle class investors.

- Further, the Dividend income is tax free, if the company is liable to dividend distribution tax.

The benefits can be availed for three consecutive years.

- Investor is free to trade / churn the portfolio after the fixed lock-in period, subject to certain conditions.

- Gains arising out of higher market valuation of RGESS eligible securities can be realized after a year viz: fixed lock-in period. Provisions exist to protect the investor from general declines in the market to a certain extent. This is in contrast to all other tax saving instruments.

- Facility for pledging stocks after the fixed lock-in period.

- For investments upto Rs.50,000 in your sole RGESS demat account, if you opt for Basic Service Demat Account, annual maintenance charges for the demat account is zero and for investments upto Rs. 2 lakh, it is stipulated at Rs 100.

- The investments can be made in installments during the financial year in which tax deduction is claimed

- Coverage of the Scheme: Investors and Investments allowed under RGESS

- Who all will be covered under the Scheme? Who is a new investor?

The Scheme is open for all New Retail Investors who have gross total income less than or equal to Rs. 12 lakh. A new retail investor is one:

- who is a resident individual (the benefit cannot be availed by HUF, corporate entities / trusts etc)

- who has not opened a Demat account and has also not done any trading in the derivative segment till RGESS account opening date or the first day of the “initial year” in which he brings in the RGESS eligible investment into the account, whichever is later.

- who has opened a Demat account and has not made any transactions in equity and /or in the derivative segment till designating such account as RGESS or the first day of the “initial year” in which he brings in the RGESS eligible investment into the account, whichever is later..

In case of joint accounts, only the first account holder will not be considered as a new retail investor. All those existing account holders other than the first demat account holder (eg. second / third account holders or other joint holders) or nominees of the existing account holders will be considered as new retail investors for the purpose of opening of a fresh RGESS account, if otherwise eligible.

In case the demat account is opened as a first holder, but there are no transactions in the equity or derivative segment, then the first account holder is eligible to be a new retail investor.

For taking the benefits under RGESS, the new retail investor will have to submit a declaration, as in Form ‘A’, to the Depository Participant (DP) at the time of account opening or designating his existing demat account.

Eligible securities, which are brought thereafter into such an account, will be automatically subject to lock-in upto a value of Rs. 50,000, unless the investor specifies otherwise through the Form ‘B’ specified in this regard.

- I am a non-resident Indian; Am I eligible for RGESS?

The Scheme is for an individual resident in India as per the provisions of the Income Tax Act.

- Can a Guardian claim RGESS tax benefit if investment is done in the name of Minor?

Yes. Guardian can claim tax benefit for investments done in the name of minor, subject to overall limit for guardian as an individual.

- I am already having physical units of mutual fund and / or Exchange Traded Funds; Am I eligible for the RGESS?

Yes. Prior investments in mutual funds and Exchange Traded Funds do not make an investor ineligible for the Scheme. However, you need to invest afresh in RGESS eligible mutual fund /ETF schemes and hold them in a demat account to avail of the benefits under RGESS.

- I possess some physical shares; Am I eligible under RGESS?

Yes. You will be considered as a new retail investor, if otherwise eligible. However, you need to make fresh investments to avail of the benefits under RGESS. You will not be eligible to claim benefits of RGESS on dematerialisation of such shares. It is advisable that you first designate / open the account for RGESS and then undertake the dematerialisation of physical shares in your custody.

- I possess some shares in the demat account; but they are of unlisted companies. Am I eligible?

No

- I have shares in demat account under the ESOP category? Am I eligible for tax benefit in RGESS?

No.

- What are the investment options available under the Scheme? What are the “eligible securities” under RGESS?

The investment options under the scheme will be limited to the following categories of securities?*:

Listed equity shares / units

- The top 100 stocks at NSE and BSE i.e., CNX-100 / BSE -100 (This does not mean that one has to trade through NSE or BSE only. If the securities constituting BSE 100 or CNX 100 are listed and traded in any new stock exchange that may come up on a later day, the same will be eligible for RGESS.)

- Equity shares of public sector enterprises which are categorized by the Government as Maharatna, Navaratna and Miniratna

- Units of Exchange Traded Funds (ETFs) or Mutual Fund (MF) schemes with RGESS eligible securities as mentioned in (a) and / or (b) as underlying, provided they are listed and traded on a stock exchange and settled through a depository mechanism)

- Follow-on Public Offers (FPOs) of (a) and (b)

- New Fund Offers (NFOs) of (c) above

Unlisted equity shares

- Initial Public Offers (IPOs) of PSUs, which are scheduled to get listed in the relevant financial year and where the government holding is at least 51% and whose annual turnover is not less than Rs. 4000 cr for each of the immediate past three years.

(*Investment criteria as applicable at the time of investment)

- Where can I get information about these eligible stocks?

The consolidated and updated list of eligible securities from time to time is published on the websites of exchanges / Depositories / The Association of Mutual Funds in India (AMFI).

For detailed information see at the relevant pages of the websites of SEBI NSE BSE, NSDL, CDSL and AMFI.

As regards eligible IPOs /FPOs/NFOs of mutual funds or ETFs, companies/mutual funds would be publishing this information in their offer documents / public advertisements.

- Why RGESS Investments are limited to top 100 stocks?

The Scheme is designed for new investors who are venturing in the equity markets for the first time. The choice of investments have been restricted to the stocks included in BSE 100 or CNX 100 and to selected PSU stocks as they generally have shown relatively, higher liquidity, and there is adequate reporting and analysis available in the market. The range of 100 stocks also provides enough scope for diversification of investments.

- When I made the investment, the particular stock was in BSE 100; thereafter it was removed from the BSE 100 list by the exchange; Is my investment still eligible for RGESS when I file my returns?

A stock has to be in BSE 100 or CNX 100 only at the time at which the investments are made. This means that even if the stock moves out of CNX 100 / BSE 100, the investor would be deemed to be compliant for RGESS. However, his rights are limited to just selling those stocks off from RGESS portfolio. If he repurchases / make additions to the existing stock, then the additional stock will not be counted as a part of the RGESS portfolio.

- When I enrolled for RGESS my annual income was below Rs. 12 lakh. However, in the subsequent year it crossed Rs. 12 lakh. Am I eligible to claim benefits?

The income limit is applicable for each of the year in which an investor is investing in RGESS. If his income crosses Rs. 12 lakh in the subsequent year, he will not be eligible to invest in that year and thereafter, provided income continues to be above Rs. 12 lakh. However, investments made in the relevant year(s) [i.e., year(s) in which investor’s income was eligible as per the scheme], will be considered eligible for claiming benefits (and no refund needs to be made for such claims).

If you receive an increment in the middle of the year by which your annual income crosses the Rs. 12 lakh barrier then all the investments made in that financial year become in-eligible.

It is the responsibility of the investor to indicate immediately to the depository through his Depository Participant when he ceases to become eligible for claiming tax benefits. Depositories would make available an application (in a specified format) that can be submitted to your Depository Participant stating that none of the fresh investments to be made in that year be kept under lock-in by the depositories. If such an investor continues to remain ineligible in the third year and if he had submitted the aforementioned application stating his ineligibility only for the second year, then, he has to submit a fresh application stating his ineligibility for the third year. Otherwise, the investor will be considered as eligible for the third year and depositories may start locking-in investments for that year.

Once the aforementioned application is submitted stating that you are not intending to avail of the benefits under RGESS for the relevant financial year(s) then the position cannot be reversed for those financial year(s).

If, after being ineligible in the second year, the annual income of the investor happens to fall below Rs. 12 lakh in the third year, then he would be considered eligible for making investments under RGESS in the third year, unless he has submitted otherwise through the aforementioned application earlier. ( i.e,, if an investor submits aforementioned application for two years, the position cannot be reversed for those financial years).

- I applied for the IPO / New Fund offer (NFO) in the month of March; However, the company / Scheme got listed in the stock exchange only in April i.e, in the next financial year. Is my investment eligible?

No, only if it is scheduled to be listed in the same financial year, the investment is eligible.

- For how many years I can avail of RGESS benefits?

RGESS benefits can be availed for three consecutive financial years, beginning with the financial year in which the investment under the Scheme was made for the first time by the investor.

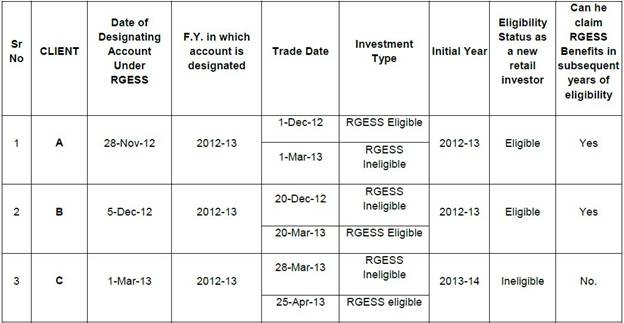

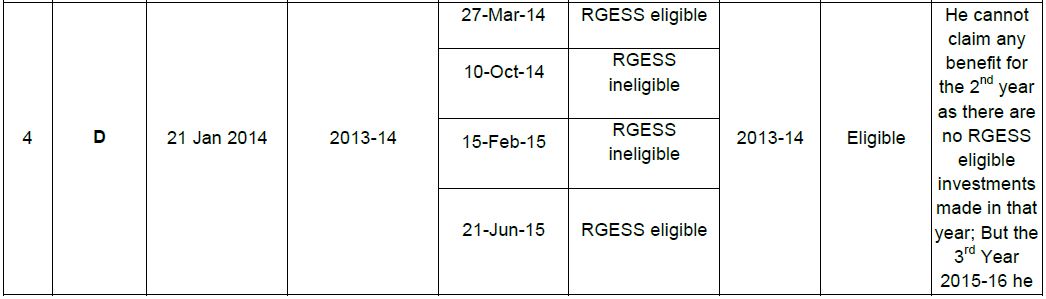

- When does counting of my three year starts? What is “initial year”?

The financial year in which the investor makes investment in eligible securities for availing deduction under the Scheme for the first time through his RGESS designated demat account is the initial year, even if the demat account was designated for RGESS in an earlier financial year.

The counting of three consecutive years starts with this initial year, i.e., the financial year in which the investments under the Scheme are made for the first time by the new investor after opening / designating the demat account for RGESS. for eg., if an investor who has opened /designated RGESS account in the FY 2012-13 does not invest in RGESS eligible securities during 2012-13 but makes investment in the FY 2013-14, then, he is eligible to invest and claim benefits during FYs 2013-14, 2014-15 and 2015-16, subject to him not making any investment in any other equity / derivative in FY 2012-13.

The investor shall also be not allowed to claim deduction under the Scheme for any previous year other than the previous year relevant to that assessment year. Thus, if the investor has forgotten to claim benefits for a particular year, he cannot carry over that benefit to the subsequent year.

- Do I have to make my first investment, after designating my account, only in eligible scrip?

A composite reading of the definition of “initial year” and “new retail investor” demands that you shall make your first investment only in RGESS eligible scrip. Thereafter, you are free to invest in other securities. This is because you will be disqualified as a “new retail investor” if the financial year in which you designate the account for RGESS is different from the financial year in which you make your first investment in RGESS eligible scrip (i.e., initial year). For instance, imagine that you have opened / designated your RGESS account in the FY 2014-15 and make investment in other equity or derivative, but fail to make any investment in RGESS eligible scrip in that year. In the next financial year, i.e., FY 2015-16, if you invest in RGESS eligible scrip, then that year is considered as the initial year. Definition of “new retail investor” is such that you should not have traded in equity or derivative as on the date of designating your account or on the first day of initial year, whichever is later. By this definition, in FY 2015-16, you are not a new retail investor and hence would be disqualified from availing RGESS benefit for any year. However, this is not an issue if you are investing in RGESS eligible scrip in the same year as you opened / designated your demat account.

- Am I mandated to make investments in all three years?

No. If the new investor does not invest in any financial year after opening /designating an account for RGESS, he shall be allowed to invest and claim benefits in the subsequent financial years, within the three year limit, however, subject to an investment limit of Rs. 50,000 in a single financial year. i.e., an investor opening/designating RGESS account in the FY 2012-13 need not necessarily invest in RGESS eligible securities during 2012-13; he is eligible to invest and claim benefits during FYs 2013-14, 2014-15 and 2015-16. This is possible only if he does not make any ineligible investments prior to the initial year.

Similarly an investor who claimed benefits under RGESS in FY 2012-13 need not necessarily invest in FY 2013-14; but can invest in FY 2014-15. However, he will not be eligible to invest in FY 2015-16. In such a scenario, he may need to submit Form B/ general application to the DP concerned for the FY 2013-14. (If there is no investment in the second year, Form B need not be submitted. The same needs to be submitted only if he does not want his investments made in the second year to be considered under RGESS.)

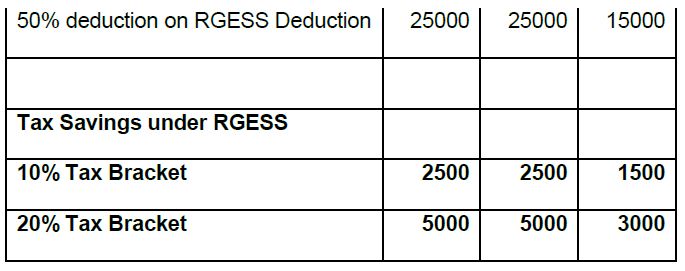

- How much tax deduction will I be eligible under RGESS?

You will be eligible to get tax deduction u/s 80CCG of the Income Tax Act, on 50% of the amount invested subject to a limit of Rs. 50,000 as investment in any financial year. Let us say, you invest Rs.50,000 under RGESS, the amount eligible for tax deduction will be Rs.25,000 from your taxable income. Let us say, you invest Rs.40,000 under RGESS, the amount eligible for tax deduction will be Rs.20,000 from your taxable income. This deduction is over and above Rs. 1 lakh limit specified under Section 80C.

In other words, for those who are in the 10% income tax bracket, savings from tax liability for investments upto Rs. 50, 000 under RGESS is Rs. 2500 (plus cess as applicable) and for those who are in the 20% income tax bracket, savings from tax liability is Rs. 5000/-(plus cess as applicable).

This deduction can be claimed for three consecutive years as mentioned above.

Illustration for tax benefit is as below

- What is the amount of deduction I am eligible for in a single financial year?

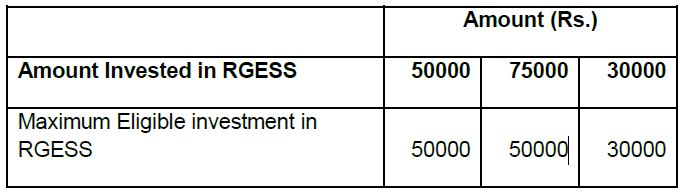

Clause (1) of Section 80CCG of the Income-tax Act has limited the allowable deductions per year to a maximum of Rs. 25,000. This means that the maximum amount of investment allowed under the Scheme is only Rs. 50,000 for any single financial year.

- I have invested less than Rs. 50,000 in a year. Can I invest more than Rs. 50,000 in subsequent years so that my total investments for three years are less than Rs. 1.5 lakhs?

No. Investments in any single financial year cannot exceed Rs. 50,000/-. If you have invested less than Rs. 50,000 in any financial year, then shortfall cannot be carried over to the subsequent year.

- What is the maximum amount that I can invest in securities market? Can I bring the same in installments?

There is no maximum prescribed limit for your investments in securities market. However, RGESS benefits will be available only for investments in eligible securities upto Rs. 50,000 per financial year upto three consecutive financial years. This investment can be made in installments during that year.

- I have already claimed tax benefit under Section 80C. Can I avail of RGESS?

Yes you can. The tax deduction for RGESS is u/s 80CCG and it is over and above Rs. 1 lakh limit specified under Section 80C. Further, it is not mandatory for citizens to exhaust the limit of Rs 1 lakh specified under Section 80C to make investments under Section 80CCG for RGESS.

- I want to invest more than Rs.50,000; how will I allocate my investments to the tune of Rs. 50 000 and claim benefit under RGESS?

You may invest any amount in a demat account designated under RGESS, but the benefit under the Scheme can be claimed only on investment up to Rs. 50,000 in a single financial year. However, you have the freedom to select the stocks to be kept under lock-in upto Rs. 50,000 for claiming benefits under RGESS. It may be noted that the depository would be automatically locking-in all the eligible securities which comes into an RGESS designated demat account during the relevant financial year (over and above what is required for meeting the flexible lock-in requirements) upto a value of Rs. 50,000. Hence, ensure that you intimate the depository participant through Form B within one month from the date of transaction, about those investments which you do not want to keep as part of RGESS investment in that year, such that you have the right to sell / pledge those securities at any time. Once an application is made through Form B, that particular security cannot be brought back under RGESS while claiming for tax benefit. In subsequent years of flexible lock-in period, if that stock is still an eligible security under RGESS provisions, then the same will be counted towards valuation of RGESS portfolio irrespective of its status as an “eligible security” while claiming benefits.

- I have purchased shares of Company ‘A’ which is an eligible security under RGESS for Rs. 70,000; How can I free the shares of the same company beyond Rs. 50,000/-?

If you have purchased shares under RGESS for Rs. 70,000/-, the depositories will place shares amounting to only Rs. 50,000/- under fixed lock-in (over and above what is required for meeting the flexible lock-in requirements). Shares amounting to Rs. 20,000 will not be under lock-in. However, if you are selective about the stocks to be kept under lock-in, then intimate the depository as mentioned in Q. No. 29

- When should I submit Form B or general application? Is there a time limit?

You need to submit Form B to the depository participant, if you wish to keep any securities outside RGESS’s terms and conditions. This needs to be submitted within one month from the date of purchase / allotment of that security.

As per the Notification, Depositories are required to submit the report to Income-tax Department regarding RGESS beneficiaries within a period of two months from the end of the relevant financial year i.e. by 31st May. Hence, to avoid wrong reporting by Depositories on your investments to Income-tax Department, you are advised to submit declaration in Form B to the depository participants for the credits received during the month of March at the earliest and preferably by April 15th. If Form B is submitted after April 15th, Depositories may consider accepting the request but not later than the expiry of one month period (April 30th), if it is satisfied that the beneficiary was prevented by sufficient cause from filing the request in time.

If you are not intending to claim benefits under RGESS for any particular year within the allowable 3 year time period (eg. in case you have crossed the income limit of Rs. 12 lakhs during a financial year and hence cannot claim benefit under RGESS for that financial year), you need to submit the general application as specified by depositories, before April 15th of the next financial year.

- Can I claim tax deduction in respect of the amount invested in eligible securities which are specified in Form B?

No.

III. Investments through Mutual funds

- What are the types of mutual funds which would be eligible for investments under RGESS?

Closed-ended Mutual Fund (MF) schemes and Exchange Traded Funds (ETF) with RGESS eligible securities as underlying would be eligible investments under RGESS, provided they are listed and traded on a stock exchange and settled through a depository mechanism. As Open-ended mutual fund schemes are not generally listed and traded on the stock exchanges, they are not eligible investments under RGESS.

- What are closed-end mutual fund schemes?

Schemes that have a stipulated maturity period are called closed-ended schemes. Investors can invest in the scheme at the time of the initial issue i.e. New Fund Offer period and thereafter can buy or sell the units of the scheme on the stock exchanges where they are listed. The market price at the stock exchange could vary from the scheme’s Net Asset Value (NAV) on account of demand and supply situation, unit holders’ expectations and other market factors. Unlike an ETF, closed ended mutual fund schemes are not frequently traded on the stock exchanges.

- How frequently is the portfolio of RGESS mutual fund scheme published?

Portfolio of close ended mutual fund schemes are published by the respective mutual fund on a monthly basis and the same shall be available on the respective mutual fund’s website. Portfolios of ETFs are published on the respective mutual fund website or the website of the stock exchanges on a daily basis.

- What is Net Asset Value (NAV) of a scheme?

The performance of a particular scheme of a mutual fund is denoted by Net Asset Value (NAV).

Mutual funds invest the money collected from the investors in securities markets. In simple words, Net Asset Value is the market value of the securities held by the scheme. Since market value of securities changes every day, NAV of a scheme also varies on day to day basis. The NAV per unit is the market value of securities of a scheme divided by the total number of units of the scheme on any particular date. For example, if the market value of securities of a mutual fund scheme is Rs 200 lakhs and the mutual fund has issued 10 lakhs units of Rs. 10 each to the investors, then the NAV per unit of the fund is Rs.20. NAV is required to be disclosed by the mutual funds on a regular basis – daily or weekly – depending on the type of scheme

- How will investors determine the value of their units in RGESS mutual fund scheme?

Mutual Funds shall compute and publish the Net Asset Value per unit of the RGESS mutual fund schemes on all business days. The same shall be available in newspapers and Association of Mutual Funds in India (AMFI) and mutual fund websites. Real time prices for ETFs would be available on the stock exchanges where the ETFs are listed and traded. In respect of mutual fund units held in demat form with NSDL, the facility to view the latest holding with valuation (alongwith NAVs) is available through IDeAS facility of NSDL. In respect of mutual fund units held in demat form with CDSL, the facility to view the latest holding with valuation ( along with NAVs) is available through ‘easi’ facility of CDSL.

- What are ETFs?

An exchange traded fund or ETF as it is popularly called is a fund comprising of a basket of securities that provides exposure to the market. ETF is traded on the stock exchange like a share. An Index ETF is based on an index which can be sector specific or broad market or international market oriented; they track the performance of an index. ETF’s are gaining popularity because they are transparent, easy to use and a low cost way to create a well-diversified portfolio. Liquidity for ETFs on the stock exchanges is provided by market makers who are called as Authorized participants.

- How to subscribe to RGESS Mutual Fund schemes?

Investors could subscribe to RGESS mutual fund schemes i.e. closed-ended mutual fund schemes or ETFs either during the New Fund Offer (NFO) period or buy in the secondary market through the stock exchanges. The NFO period could be for up to 30 days and the opening and closing dates will be mentioned on the Key Information Memorandum (KIM) of the mutual fund scheme. Thereafter, the units can be purchased/sold on a continuous basis (subject to suspension of trading/lock-in period) on stock exchanges on which the units of RGESS mutual fund schemes are listed, during the trading hours like any other publicly traded stocks. (whenever you are applying for the subscription of RGESS Mutual Fund schemes, remember to write your demat account number (DP ID and Client ID) on the application form.)

- Are RGESS mutual fund Schemes available for investment to regular investors who are not eligible for RGESS or who do not intend to avail of tax benefits under RGESS?

Yes; An RGESS eligible mutual fund or ETF Scheme is available for investment to any investor looking to invest in equity schemes for the long term. However, tax benefits can be claimed only if the units are subscribed through and held in the designated demat account and other eligibility conditions are satisfied by the investors.

- Is a demat account compulsory for investing in RGESS mutual fund?

Demat account is compulsory for investors who wish to avail tax benefits under RGESS and the demat account details should be specified in the application form. Those investors who are not claiming tax benefits can hold units of RGESS eligible mutual fund schemes in the form of account statement.

- What documents / information do I need to submit with my RGESS mutual fund application form at the time of subscription during the NFO?

Duly filled-in application form of the RGESS mutual fund scheme (which is a part of the KIM), cheque drawn in the name of the scheme, and details of the demat account i.e. Client ID and DP ID.

- What are the Plans offered by mutual fund schemes?

Mutual fund schemes offer two plans i.e. Regular Plan and Direct Plan. Direct Plan is only for investors who purchase /subscribe units in a scheme directly with the mutual fund and is not routed through an AMFI Registration Number (ARN) Holder or a distributor or a broker. Expenses charged by the Direct Plan will be lower than the Retail Plan to the extent of selling and distribution costs charged in the Retail Plan.

- What are the Options available under each of the above Plans?

Mutual fund schemes generally offer two options i.e. Dividend and Growth. Dividend Option are meant for investors seeking regular dividend income and Growth Options are meant for investors seeking long term capital appreciation

Dividend Option: Under this Option, the Trustee reserves the right to declare dividend under the scheme depending on the net distributable surplus available under the Option. It should, however, be noted that actual declaration of dividends and the frequency of distribution will depend, inter-alia, on the availability of distributable surplus and will be entirely at the discretion of the Trustees or any Committee authorized by them.

Growth Option: Under this option there will be no distribution of income by way of dividends. All Income earned and realized profit in respect of a unit issued under that will continue to remain invested in the scheme and shall be deemed to have remained invested in the option itself, which will be reflected in the NAV.

- What is the frequency of dividends that will be declared in RGESS MF scheme?

The Trustees of the respective Mutual Fund reserve the right to declare a dividend. The quantum and frequency of distribution are entirely at their discretion.

- Do mutual fund schemes pay income tax?

Incomes of mutual fund schemes are exempt from income tax. Currently, RGESS mutual fund schemes are not required to pay dividend distribution tax on dividends distributed to investors as they are equity oriented mutual fund schemes.

- Are dividends distributed by mutual fund schemes taxed in the hands of investors?

Currently, dividends distributed by mutual fund schemes are exempt from income tax in the hands of investors.

- Where can I find the list of RGESS mutual fund schemes?

List of RGESS mutual fund schemes are available under ‘investors zone” in www.amfiindia.com and also on the websites of NSE and BSE. Details of RGESS mutual fund schemes will also be available on the websites of respective mutual funds.

- Where should I submit my RGESS mutual fund application form during the NFO?

RGESS application form can be submitted to any of the official points of acceptance of the respective mutual fund which will be mentioned in the KIM and on the mutual fund’s website. (Remember to quote your demat account number on the application form.)

- When will the allotment be done for RGESS mutual fund?

Allotment of units for RGESS mutual fund schemes will be done within 15 days from the closure of the NFO period

- How will I be intimated about the allotment?

Mutual fund will send an Allotment Advice to investors. Additionally, the Depository Participant in which the investor holds the demat account would also send a statement for unit allotment. Depositories would also send an SMS upon receipt of credit of mutual fund units in your demat account, if you have registered your mobile number while opening your demat account.

- When would the refund be done for rejected applications?

For RGESS eligible Mutual Fund scheme, the refund will be done within fifteen days from the closure of the initial subscription/ NFO

- Is there an option to exit from RGESS mutual fund before 3 years?

Since RGESS mutual fund schemes are closed-ended mutual fund schemes / ETFs, investors cannot redeem their units through the mutual fund. Investors have an exit option (subject to lock-in period) by trading on the stock exchanges, since the units will be listed and traded on the stock exchanges. All closed-ended mutual fund schemes and ETFs are listed on the stock exchange. However, it is the responsibility of investors availing of RGESS tax benefits to ensure that they are in compliance with the lock-in requirements under RGESS.

- What happens if investors do not trade and hold the units in a closed-ended mutual fund scheme till the maturity of the scheme?

On the maturity date, all units under the scheme will be compulsorily, and without any further act by the unit holders, redeemed at the applicable NAV of that day. For the units held in electronic/ demat form, the units will be extinguished with the depository and the redemption amount will be paid to the unit holders on the maturity date, at the prevailing NAV on that date.

- Is Systematic Investment Plan (SIP) available in RGESS?

As RGESS mutual fund schemes are either closed-ended mutual fund schemes or ETFs, subscriptions into such schemes by mutual funds can only be accepted during the New Fund Offer period. Therefore, Systematic Investment Plans, whereby investors agree to contribute monthly subscriptions during a defined future period directly to a mutual fund post the New Fund Offer period cannot be offered to investors under RGESS scheme. Post closure of the NFO, units can only be bought on the stock exchanges where they are listed.

- Can an investor switch existing Mutual Fund units to RGESS Scheme? Will I be eligible for tax benefits?

Yes – Eligible investors can submit switch request into RGESS mutual fund schemes from any other scheme of the mutual fund during the NFO period. However, to avail tax benefit under RGESS scheme, the investor needs to ensure that the allotment of units in RGESS mutual fund scheme is done in the designated demat account and needs to comply with the guidelines prescribed under RGESS.

- What is the expense ratio charged under RGESS Mutual Fund scheme?

The annual recurring expenses charged by a RGESS Mutual fund scheme shall be within the limits specified under the SEBI (Mutual Funds) Regulations, 1996. However, Direct Plans will have lower expense ratio than Regular Plan of the Scheme. The expenses under Direct Plan shall exclude the distribution and commission expenses. The maximum limit of recurring expenses that can be charged to the Schemes would be as per Regulation 52 of the SEBI (MF) Regulation, 1996. Investors are requested to refer to the section on – “FEES and EXPENSES” contained in the KIM which will have details of the expenses proposed to be charged. For the current actual expenses being charged, the investor should refer to the website of the Mutual Fund.

- What will be the entry / exit load charged to investors, if invested in RGESS Mutual Fund schemes?

Entry Load – NIL. However, as per the guidelines issued by SEBI, a transaction charge (for existing investors in a Mutual Fund:- Rs. 100/- and for a first time investor in Mutual Funds:- Rs. 150/-) per subscription of Rs. 10,000/- and above is allowed to be paid to the distributors of the Mutual Fund products.

Exit Load – Not Applicable (As the RGESS mutual fund schemes will be in the nature of closed end schemes, units under the schemes cannot be directly redeemed with the Mutual Fund).

- Whom can the investor contact for any complaint regarding RGESS Mutual Fund units?

The investor can approach the respective Mutual fund or Registrar and Transfer Agents (RTA) of the respective mutual fund to register their complaints. Investors can also mail their query to asksebi@sebi.gov.in. Details of the offices of the mutual fund and their RTA would be available on the mutual fund’s website. SEBI commenced a new web based centralized grievance redress system called as SCORES (SEBI Complaints Redress System) on June 8, 2011. In the new system, all the activities starting from lodging of a complaint till its closure by SEBI are online in an automated environment and the status of every complaint can be viewed online in the above website at any time. An investor, who is not familiar with SCORES or does not have access to SCORES, can also lodge complaints in physical form. Such complaints are scanned and uploaded in SCORES for processing. In view of above, all grievances received will be in electronic mode with facility for online updation of Action Taken Reports by the users.

IV Participating in the Scheme: Procedural and Operational issues

- How to make RGESS eligible investments?

Open a new demat account with any DP and designate it under RGESS or designate your existing demat account under RGESS through Form A. If you want to avail of Basic Service Demat Account facility, you may inform your DP to designate your account accordingly.

You may approach any SEBI registered stock broker for opening a trading account for making investment in any eligible stocks in the stock market or for applying for eligible IPOs.

In case you are investing in mutual funds through any distributor, you need to simply provide your demat account details like Demat Account Number and DP ID for receiving credit of the mutual fund units into the demat account

For investing in any IPO/NFO of the eligible securities, you can subscribe for the same and provide your demat account details like Demat Account Number and DP ID for receiving credit of the eligible securities into the demat account.

- I opened/activated the demat account for the purpose of availing of RGESS benefits. However, I forgot to submit Form A and started transacting through my account. Will I be considered ineligible for claiming benefits?

If you have made investments in that demat account prior to submission of Form A, you will be considered ineligible, even if you are eligible to be a new investor and might have opened that demat account with the intention of claiming tax benefits. This is because new investors are technically defined as someone who has not done any transaction in equity or derivative before opening such account / designating such demat account for RGESS (through Form A)

- Mr. A has a demat account and he does an off market transfer of eligible stocks into Mr.B’s account, who is a 1st time retail investor but still has not designated his account for RGESS. Is Mr. B eligible for RGESS?

No.

- Is credit received in my demat account through dematerialisation eligible for claiming benefits under RGESS?

No. It will not be treated as a fresh investment for claiming deduction. However, in the years of flexible lock-in (i.e., after the first year) all RGESS eligible securities would be counted towards checking for compliance of the investor with the Scheme, irrespective of whether it was acquired off market or came in through dematerialization.

- What will be the mode of holding eligible securities?

The mode of holding eligible securities under RGESS will be in a ‘Demat account’. You cannot hold securities in physical form or with a Mutual Fund directly to enjoy the benefits of RGESS.

- Should I need to get my mutual fund / ETF units also in demat form?

Yes. For getting your mutual fund units in demat form, make a request with your mutual fund or RTA (Registrar and Share Transfer Agent) of the mutual fund. For more details please see the instructions / guidance of CDSL and NSDL.

- I have purchased RGESS eligible mutual fund units in physical mode; Will I be eligible for tax benefit if I convert it to demat at a later date?

No. Only the securities bought through stock exchange or credited by mutual fund houses into your account through corporate action are eligible for RGESS benefits.

- Is there any need for the investor to open a dedicated demat account for availing of RGESS benefits? Can I hold other securities i.e., other than eligible securities in my demat account designated for RGESS?

There is no need to open a separate dedicated account for availing of the RGESS benefits. The demat account through which RGESS benefits are being availed of can be used to keep shares/ securities other than RGESS-compliant securities. Investments in shares other than RGESS-compliant securities shall not be subject to the conditions of RGESS, nor shall be counted for extending the tax benefits under RGESS. However, it is strictly advised that after designating or opening your account under RGESS, you may do your first transaction in an RGESS eligible scrip only. (may see Q No. 22)

- How to open RGESS demat account with a Depository Participant (DP)?

You may approach any registered DP to open a demat account under RGESS. The list of DPs registered with NSDL and CDSL may be seen here.

You are required to fulfill the Know your client (KYC) norms prescribed by SEBI, if not done earlier, by submitting proof of identity, proof of address, etc. and provide PAN to the DP with whom you wish to open a demat account along with a declaration in prescribed format (i.e., ‘Form A’) for availing RGESS benefits.

For more details see the FAQ given by NSDL and CDSL

- How to open a trading account?

You can contact a broker (trading member) or a sub broker registered with SEBI for carrying out your transactions pertaining to the capital market. See the list of registered brokers / sub brokers on the SEBI website.

- What are the documents I need to bring for opening a demat / trading account?

You have to submit the following with the prescribed account opening form. In case you want to open account jointly with other person(s), following should be submitted for all the account holders.

Self-attested copy of PAN card and copies of passport size photograph is mandatory for all. Copies of all the documents submitted by the applicant should be self-attested and accompanied by originals for verification. In case the original of any document is not produced for verification, then the copies should be properly attested by entities authorized for attesting the documents.

i Proof of Identity (POI)

Passport

- Voter ID Card

- Driving license

- PAN card with photograph

- Aadhar (Unique ID) letter

- Identity card/document with applicant’s Photo, issued by

- a) Central/State Government and its Departments,

- b) Statutory/Regulatory Authorities,

- c) Public Sector Undertakings,

- d) Scheduled Commercial Banks,

- e) Public Financial Institutions,

- f) Colleges affiliated to Universities (this can be treated as valid only till the time the applicant is a student),

- g) Professional Bodies such as ICAI, ICWAI, ICSI, Bar Council etc., to their Members; and

- h) Credit cards/Debit cards issued by Banks.

ii Proof of Address (POA)

- Ration card

- Passport

- Voter ID Card

- Driving license

- Bank passbook

- Verified copies of utility bills like Electricity bills, gas bills (not more than three months old)/

Residence Telephone bills (not more than three months old)/ Registered lease or sale agreement of residence

/ Flat maintenance bill / insurance copy

- Bank account statement / pass book

- Self-declaration by High Court & Supreme Court judges, giving the new address in respect of their own accounts.

- Proof of address issued by any of the following: Bank Managers of Scheduled Commercial Banks/

Scheduled Co-Operative Bank/Multinational Foreign Banks/ Gazetted Officer/Notary public

/ Elected representatives to the Legislative Assembly/Parliament/Documents issued by any

Govt. or Statutory Authority.

- Identity card/document with address, issued by

- a) Central/State Government and its Departments,

- b) Statutory/Regulatory Authorities,

- c) Public Sector Undertakings,

- d) Scheduled Commercial Banks,

- e) Public Financial Institutions,

- f) Colleges affiliated to universities (this can be treated as valid only till the time the applicant is a student); and

- g) Professional Bodies such as ICAI, ICWAI, Bar Council etc., to their Members.

List of people authorized to attest the documents: Notary Public, Gazetted Officer, Manager of a

Scheduled Commercial/ Co-operative Bank or Multinational Foreign Banks (Name, Designation &

Seal should be affixed on the copy).

You must remember to take original documents to your DP / trading member for verification. Your DP /

trading member will carry-out “in-person verification” of account holder(s) at the time of opening your account.

You should remember to obtain a copy of the agreement and schedule of charges for your future reference.

Your DP / trading member may ask an additional proof of identity/address.

- I belong to PAN exempt category (resident of Sikkim); Can I open an RGESS account without PAN?

For availing benefits under RGESS, PAN is made mandatory even if you belong to PAN exempt category.

See here for more details as to how to get a PAN card.

- Should I ask for internet access to my trading and demat accounts?

Yes, it is preferable. This would facilitate you to keep a real time track of your account and the value of securities

held therein.

- Can I designate an existing demat account under RGESS?

Yes, provided you are eligible as a ‘new retail investor’ under RGESS. To designate your existing demat account under RGESS you need to submit a declaration in prescribed format (i.e., ‘Form A’) to your DP.

- Where will I get ‘Form A’ Form “B” etc?

You can get ‘Form A’ and Form ‘B’ from your DP or download it from the website directly. Click here to download. Form A & B can be submitted either in electronic (if the facility exists) or physical format. Depository will also make available the application to be submitted for seeking exemption from RGESS for any particular year(s).

- Can I designate or open more than one demat account for RGESS?

No. You can have only one demat account under RGESS, across depositories (i.e., NSDL / CDSL).

- Is there a low cost demat account for RGESS?

With a view to achieve wider financial inclusion, encourage holding of demat accounts and to reduce the cost of maintaining securities in demat accounts for retail individual investors, it has been decided on 27 August 2012 that all depository participants (DPs) shall make available a “Basic Services Demat Account” (BSDA) with limited services to all the individuals who have or propose to have only one demat account, where they are the sole or first holder, with value of securities held in that demat account not exceeding Rupees 2 lakhs at any point of time. For such demat accounts no Annual Maintenance Charges (AMC) will be levied by DPs, if the value of holding is upto Rs. 50,000. For the value of holding from Rs 50,001 to Rs 200,000, AMC is stipulated to not exceed Rs 100. The first time investors can make use of BSDA and reduce their cost of operations in the equity market by designating their RGESS account also as a BSDA account. The form for designating the account as a BSDA account can be downloaded from the websites of depositories – NSDL & CDSL

The comparative charges of opening demat accounts with various Depository Participants may be seen from the respective websites of Depositories – NSDL and CDSL.

- What are the do’s and don’ts while operating in securities market?

Please see the SEBI guidelines in this regard. Please see the websites of Exchanges – BSE and NSE for safety advices. See the investor guides of NSDL and CDSL too.

SEBI maintains an updated, comprehensive website for education of investors (www.investor.sebi.gov.in). Please go through the materials given in there, before making investments in securities market.

- How can I register my complaints with respect to my transactions in securities market?

In the event of any complaint you should first approach the concerned company/ intermediary against whom you have a complaint / grievance. SEBI has directed all the stock exchanges, registered brokers, sub-brokers, depositories, mutual funds and listed companies to make a provision for a special email ID of the grievance redressal division/ compliance officer for the purpose of registering complaints by the investors.

If the complaint is not resolved at the level of company / intermediary you may approach the concerned depository / Exchange.

Depositories and Stock Exchanges have set up investor grievance redressal cells for fast redressal of investor complaints relating to securities markets. Exchanges have set up an Investor Protection Fund (IPF) to meet the claims of investors against defaulter brokers; The Exchanges and depositories also assist in arbitration process between brokers/ depository participants and investors.

Please see the websites of Exchanges – BSE and NSE – and Depositories – NSDL & CDSL -regarding the details of investor grievance redressal mechanisms.

If the complaint is not resolved at the level of exchanges / depositories, you may escalate the complaint to the market regulator, SEBI. SEBI also directly takes up complaints related to issue and transfer of securities and non-payment of dividend with listed companies. In addition, SEBI also takes up complaints against the various intermediaries registered with it like mutual funds, stock brokers and related issues. SEBI has also set up a mechanism for redressal of investor grievances arising from the issue process.

SEBI commenced a new web based centralized grievance redress system called as SCORES (SEBI Complaints Redress System) on June 8, 2011. In the new system, all the activities starting from lodging of a complaint till its closure by SEBI are online in an automated environment and the status of every complaint can be viewed online in the above website at any time. An investor, who is not familiar with SCORES or does not have access to SCORES, can also lodge complaints in physical form. Such complaints are scanned and uploaded in SCORES for processing. In view of above, all grievances received will be in electronic mode with facility for online updation of Action Taken Reports by the users.

Investors can write/ call/ mail their query to asksebi@sebi.gov.in and their queries are replied.

The toll free helpline service numbers 1800 22 7575 / 1800 266 7575 are available to investors from all over India and is in 14 languages viz. English, Hindi, Marathi, Gujarati, Tamil, Bengali, Malayalam, Telugu, Urdu, Oriya, Punjabi, Kannada, Assamese and Kashmiri. The toll free helpline service is available on all days from 9:30 a.m to 5:30 p.m (excluding declared holidays). Further, SEBI has opened local offices at Bangalore, Bhubaneshwar, Chandigarh, Guwahati, Hyderabad, Indore, Jaipur, Kochi, Lucknow and Patna to provide the service to the investors in these localities.

You can also approach Capital Market Division, Department of Economic Affairs, Ministry of Finance for resolving your grievances / submitting your suggestions.

- If the RGESS account holder has expired and if the securities are under fixed lock-in, can it be transferred to the nominee / legal heir?

Yes; Depositories would enable such transfers upon request from the legal heir / nominee even though the securities are under fixed lock-in.

The legal heir / nominee can file for the tax exemption as a representative assessee for the expired RGESS beneficiary, for the year in which the expired RGESS account holder has not availed of the tax exemption on his RGESS investments. However, the legal heir cannot claim benefits on his behalf for the subsequent years.

If the transferee /legal heir is also an RGESS beneficiary, he would be entitled to receive the securities from the account of the expired beneficiary.

V. Implementation of Lock-in conditions and Valuation of securities under RGESS

- What will be the basis for valuation of initial investment made under RGESS for availing tax benefit?

Valuation of initial investments i.e., upto Rs.50,000, for availing tax benefits under RGESS will be based on the cost of acquisition of eligible securities. This means that it excludes brokerage charges, Securities Transaction Tax, stamp duty, service tax and all taxes which are appearing in the contract note issued by the stock broker. The cost of acquisition (or the price at which the specified quantity was purchased) is taken by the depositories directly from the stock exchange on which the transaction has been done. You may verify the entries made by the depositories as “initial investment under RGESS” using the information given in the contract note provided to you by your broker.

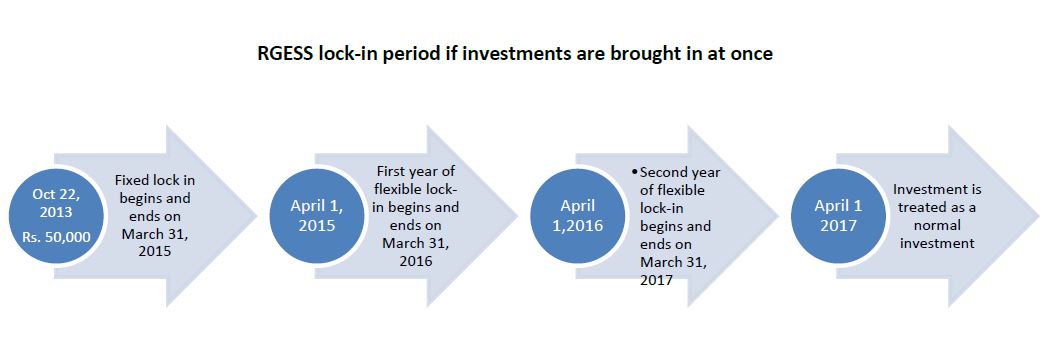

- What is the holding period for investments made under RGESS?

Investment holding period under RGESS is three years which includes ‘Fixed Lock-in’ and ‘Flexible lock-in’. This investment holding period is applicable for all year(s) in which investment is made under RGESS.

Example:

Let us say, you have purchased eligible securities worth Rs. 50,000 on 31 December 2013 in a RGESS designated demat account. The eligible securities will be in ‘Fixed lock-in’ till 31 March 2015 and for flexible lock-in till 31 March 2017.

In case you intend to sell investment made under RGESS within three years, it can be done only after completion of ‘Fixed Lock-in’ period, subject to certain conditions. The lock-in time lines in case of investments made at once and in installments are illustrated in the below mentioned graph.

RGESS lock-in period if investments are brought in at once

RGESS lock-in period if investments are brought in as installments

‘Fixed Lock-in’ period shall commence from the date of credit of first set of eligible securities in the relevant financial year and end on the 31st day of March of the year immediately following the relevant financial year. . Investor is not allowed to sell / pledge securities during this period.

- What is ‘Fixed Lock-in’ period? Has the concept changed from that adopted during FY 2012-13?

In FY 2012-13, the concept of fixed lock-in and hence, the flexible lock-in were on a rolling basis. For instance, Fixed Lock-in’ period commenced from the date of purchase of first set of eligible securities in the relevant financial year and end one year from the date of purchase of the last set of eligible securities (in the same financial year). For instance, if you had purchased the first set of eligible securities worth Rs. 20,000 on December 25, 2012 and next set of eligible securities worth Rs. 20,000 on December 31, 2012 in a RGESS designated demat account, then the ‘Fixed lock-in’ period for both set of eligible securities will start from December 25, 2012 and will end on December 30, 2013. Two years from December 30, 2013 i.e., on 30 December 2015 the flexible lock-in would have come to an end.

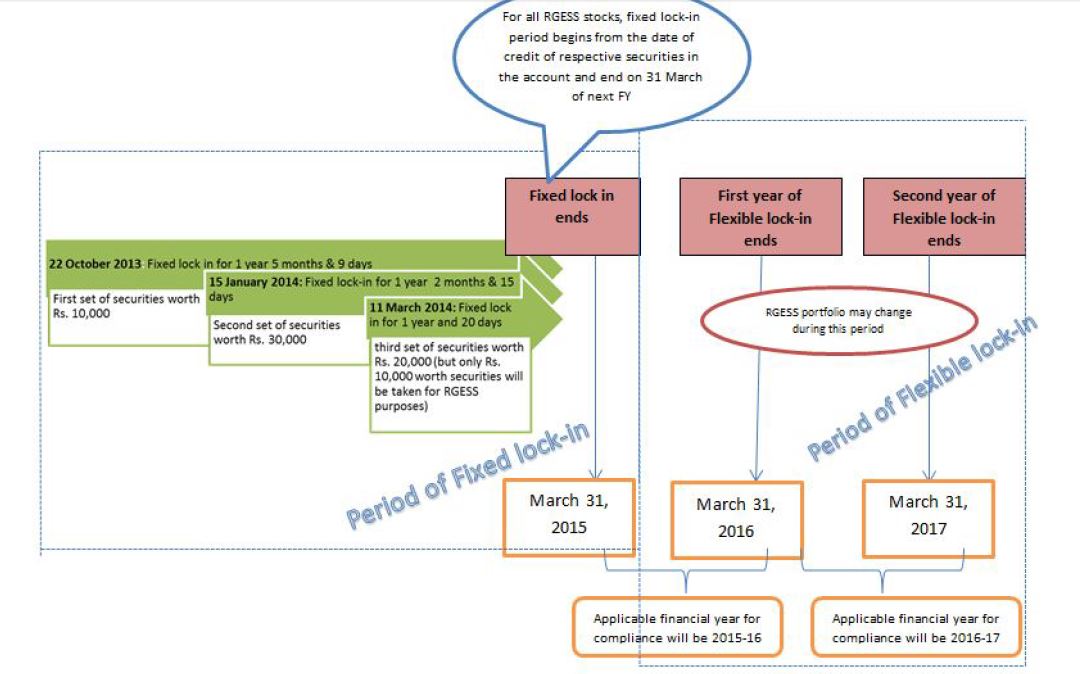

When RGESS was extended for 3 years in FY 2013-14, this necessitated a change in the concept of Fixed lock-in and hence in flexible lock-in. Presently both the lock-in periods are calculated on a financial year basis.

Example:

If you have purchased first set of eligible securities worth Rs. 20,000 on 22 October, 2013 and next set of eligible securities worth Rs. 20,000 on 11 March, 2014 in a RGESS designated demat account, then the ‘Fixed lock-in’ period for both set of eligible securities will start from 22 October, 2013 or 11 March 2014, as the case may be, and will end for both on 31 March 2015.

- I started my RGESS investment in FY 2012-13; Am I also bound by the new definition of fixed lock-in?

Yes.

- When the lock-in period does start? From the date of purchase or from date of credit of securities in the demat account?

As there can be a time gap between the date of purchase and date of credit, the fixed lock-in period will commence from the date of ‘credit’ of such securities in the demat account during the relevant financial year

- Won’t the above method of calculating fixed lock in result in lock-in for more than three years?

Yes, if the investment is made in the beginning months of a financial year, the investment may be locked in for more than three years. Since the investor is given the flexibility (of no lock-in) for around 90 days in each of the flexible lock-in period, this extra lock-in period in the first year is sort of compensated for.

- Can I sell / pledge eligible securities declared for RGESS during ‘Fixed Lock-in’ period?

No. You are not allowed to sell, pledge or hypothecate eligible securities during ‘Fixed Lock-in’ period.

- What is ‘Flexible Lock-in’ period?

The period of two years beginning immediately after the end of the fixed lock-in period shall be called the ‘Flexible Lock-in’ period.

- Can I trade / sell during flexible lock-in period?

During ‘Flexible lock-in’ period, you can trade (sell/buy) the eligible securities and remain eligible to claim tax benefit under RGESS, provided that, the RGESS demat account is compliant for a cumulative period of a minimum of two hundred and seventy days during each of the two years of the flexible lock-in period. This means that you get almost a quarter of the year to churn your portfolio.

- How the valuation of securities is done during the flexible lock-in period?

For checking compliance with the Scheme after any sale is done from the RGESS portfolio during the flexible lock-in period, the following balances of securities will be considered at the closing price as on the previous day of the date of ‘trading’ (which is what get reflected as the value of the portfolio in the demat account of the investor on any day during trading hours; This is done to facilitate the decision making by investors). The date of trading is obtained by the depositories directly from the stock exchanges.

- The balances of securities which were under fixed lock-in in the previous financial years (and are presently in flexible lock-in periods), irrespective of its status as an ‘eligible security’ as on the date of valuation (This means that even if the security had gone out of the CNX 100 or BSE 100 list, if it was a part of the fixed lock-in and still retained in the account it would be considered towards the valuation of RGESS portfolio).

- The balances of securities which are appearing in the list of eligible securities as on the date of valuation, even though not forming part of the securities which were held under fixed lock in. These securities could have been bought by the investor during fixed lock-in period or subsequently.

- Additional credit of securities received through Bonus/Rights as part of corporate action on eligible securities.

The securities currently kept under fixed lock-in will not be counted towards calculation of compliance with flexible lock-in period. (i.e., any gain in valuation of securities presently kept under fixed lock-in cannot be utilized for meeting the requirements of currently running flexible lock-in period(s)).

- How does DPs allot the fresh investments made in subsequent years?

Any credit of eligible securities into the demat account in subsequent years will first be considered for compliance with the requirement of flexible lock-in of earlier previous year (s) and the remaining securities will be considered as fresh investment of the financial year in which the investment is made and will be eligible for deduction under sub-section (1) of Section 80CCG of the Act in that financial year.

For the purpose of valuation of investment during the flexible lock-in period, the closing price as on the previous day of the date of trading shall be considered, while original investments on which benefits are claimed will be valued at the acquisition cost.

In a scenario where the investment done in the second financial year has to be allocated partly towards compliance with the first year and partly towards fixed lock-in as investments for the second year, the securities allocated towards compliance with the flexible lock-in period for the previous years would be valued on the basis of closing price of the previous day of the date of trading / execution as the case may be and the securities allocated towards RGESS investment would be valued on the basis of trading price.

e.g. If there is a non-compliance to the extent of Rs. 10,000 towards first financial year and in the second financial year the investor purchases 1000 securities @ Rs. 20 (trading price) for which the closing price before trading day was Rs. 25, then 400 securities (25*400=10000) will be allocated towards compliance and remaining 600 securities @20 = Rs. 12,000 will be under fixed lock-in as investments for the second year.

- After first year, if the value of the RGESS eligible portfolio crosses the first year’s investment value can the excess value be considered as the new investment done in the second year?

Section 80CCG of the IT Act mandates that securities should have been acquired by the investor in the relevant previous year; In view of the same, surplus investments made in the previous years are not carried over as fresh investments for the subsequent year for claiming benefits under RGESS for that year. However, if there are eligible securities they will be counted towards compliance for the flexible lock-in period.

- Is there a difference in the valuation of RGESS eligible securities as compared to the general valuation principle adopted by Depositories?

Yes. Valuation of initial investments for claiming tax benefits under RGESS is mentioned in Q. No. 80. The valuation criterion for the securities during the flexible lock-in period is mentioned in Q. No. 89.

Depositories generally value the securities in a demat account based on the closing price of the securities at the exchanges (for CDSL closing price at BSE is taken; for NSDL closing price at NSE is taken) for that day. The same is updated after the close of market hours every day. Since RGESS valuation is done at the actual price of acquisition for the initial investment and at previous day’s closing price during flexible lock-in period, it is different from the general valuation done by depositories for other securities.

However, for RGESS beneficiaries, depositories will show separately the value of initial investment under RGESS and the value of his/ her RGESS portfolio on a day to day basis.

- How the three year lock-in condition is implemented?

The total lock-in period for investments under the Scheme would be three years including a fixed lock-in period of one year, commencing from the date of credit of securities in your demat account under RGESS.

After the fixed lock-in period, investors would be allowed to trade, in furtherance of the goal of promoting an equity culture and also as a provision to protect them from adverse market movements or stock specific risks, as also to give them avenues to realize profits.

Investors would, however, be required to maintain their level of investment during these two years at the amount for which they have claimed income tax benefit or at the value of the portfolio before initiating a sale transaction, whichever is less, for at least 270 days in a year. This process is clarified below:

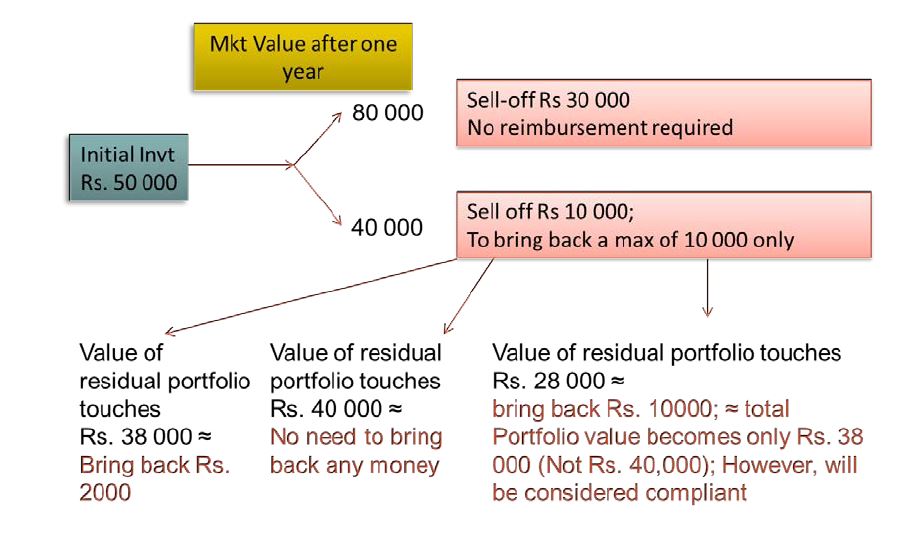

- The RGESS account will be deemed to be compliant unless such a trade (sale) is done that brings the value of the RGESS portfolio, on the date of sale, below the amount for which benefits have been claimed under RGESS, when valued at the closing price of the stocks / units on the preceding day of trading. This means that as long as the market valuation of all the RGESS eligible securities in your account (excluding those which are currently in the fixed lock-in period) is above the amount for which benefits have been claimed, you can sell off securities above such level, without necessitating you to further purchase any RGESS eligible securities. Further, even if the market valuation of all RGESS eligible securities in your account is below the amount for which benefits have been claimed, if you have not sold off any security, you will still be deemed compliant with the Scheme; the clock ticks in only if a ‘sale’ is done from the RGESS eligible securities. This gives protection from general market declines.

- In case of any sale during the flexible lock-in period by which the value of the cumulative RGESS portfolio (i.e, value of securities kept in all the currently running flexible lock-in periods including value of other RGESS eligible securities not under fixed lock-in) goes below the cumulative amount for which tax benefits have been claimed (i.e., sum of all tax claims made in all the relevant years corresponding to the presently running flexible lock-in periods), then the account would be deemed to be RGESS compliant only from the day on which the value of the RGESS portfolio becomes at least equivalent to the amount for which tax benefits have been claimed or the value of the RGESS portfolio before such sale, whichever is less. This may happen in any of the following manner, in part or full:

- Due to market movements, the cumulative value of the remaining RGESS portfolio becomes not less than the cumulative amount for which RGESS benefits have been claimed or the value of cumulative RGESS portfolio before the sale of such securities, whichever is less.