Standard Operating Procedure on TDS under GST

Standard Operating Procedure on TDS under GST-FAQ and Ready Reckoner for guidance of DDOs and other deductors under GST by Law Committee of GST Council

Central Board of Indirect Taxes and Customs has issued Notification No. 50/2018 – Central Tax making the TDS provisions under section 51 of GST applicable from 01.10.2018 . The Government has also issued a Guidelines for Deductions and Deposits of TDS by DDOs under GST.

Now, Law Committee GST Council has issued Standard Operating Procedure (SOP) on TDS under GST. It is a ready reckoner for guidance of DDOs and other deductors under GST, ot also contains a FAQ on TDS provisions under GST Law.

Also Refer FAQ issued on TCS under GST.

1. Introduction:

The concept of Tax Deduction at Source (TDS) was there in the erstwhile VAT Laws. GST Law also mandates Tax Deduction at Source (TDS) vide Section 51 of the CGST/SGST Act 2017, Section 20 of the IGST Act, 2017 and Section 21 of the UTGST Act, 2017. GST Council in its 28th meeting held on 21.07.2018 recommended the introduction of TDS from 01.10.2018. [ Refer Notification No. 50/2018 – Central Tax ]

Following would be the deductors of tax in GST under section 51 of the CGST Act, 2017 read with notification No. 33/2017-Central Tax dated 15.09.2017:

(a) a department or establishment of the Central Government or State Government; or

(b) local authority; or

(c) Governmental agencies; or

(d) an authority or a board or any other body,-

(i) set up by an Act of Parliament or a State Legislature; or

(ii) established by any Government,

with fifty-one per cent. or more participation by way of equity or control, to carry out any function; or

(e) a society established by the Central Government or the State Government or a Local Authority under the Societies Registration Act, 1860 (21 of1860); or

(f) public sector undertakings.

The procedures of TDS along with related legal provisions are discussed herein below for the understanding of the stakeholders including the Drawing and Disbursement Officers (DDOs) who are required to deduct tax in accordance with the provisions of the GST Laws.

2. Relevant provisions of TDS in GST and effective date:

2.1 Provisions of Law:

GST Laws provide for tax deduction at source (TDS) by the specified category of persons (herein after referred to as ‘the deductor’) from the payment made or credited to the supplier of taxable goods or services or both (herein after referred to as ‘the deductee’) at a prescribed rate.

2.2 Effective date:

Notification No. 33/2017 – Central Tax dated 15.09.2017 was issued by the CBIC to enable registration of tax deductors. However, Government suspended the applicability of TDS till 30.09.2018. Now, it has been decided that the TDS provision would be made operative with effect from 01.10.2018. Notification No. 50/2018-Central Tax dated 13.09.2018 has already been issued in this regard by CBIC. Similar notifications have been issued by respective State Governments.

2.3 Brief Diagrammatic presentation of the TDS provisions in GST:

2.4 Concept of Supply in GST

Section 7 of the CGST/SGST Acts 2017: “……..”supply” includes –(a) all forms of supply of goods or services or both such as sale, transfer, barter, exchange, license, rental,lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business;………”

⇒ Supply in GST covers both supply of goods as well as supply of services by vendors/suppliers to the Government Departments, local authorities and other recipients as listed in para 1 (a) to (f) above.

Examples of supply of goods to Government/local authorities:

Procurement of stationery items, toilet articles, towels, furniture, air-conditioning machines, electrical goods, books and periodicals & medicines, etc.

Examples of supply of services to Government/local authorities:

Procurement of security services, car rental services, generator rental services, rental services like office building/land taken on rent, maintenance services, rental of machinery, etc.

⇒ There may be supplies which are composite in nature i.e. taxable supplies of goods and services or both which are naturally bundled and supplied in conjunction with each other in the ordinary course of business [Section 2(30) refers].

Examples of Composite supplies to Government/local authorities:

Works Contract services such as road, bridge, building development / renovation / repairing / maintenance services involving supplies of both goods and services.

⇒ Taxable Supply means supply of goods or services or both which is leviable to tax under GST [Section 2(108) refers]

⇒ Exempt supply means supply of any goods or services or both which attracts nil rate of tax or which may be wholly exempt from tax under section 11 of the CGST / SGST Acts or under section 6 of the IGST Act, and includes non-taxable supply. [Section 2(47) refers]

3. When tax deduction is required to be made in GST:

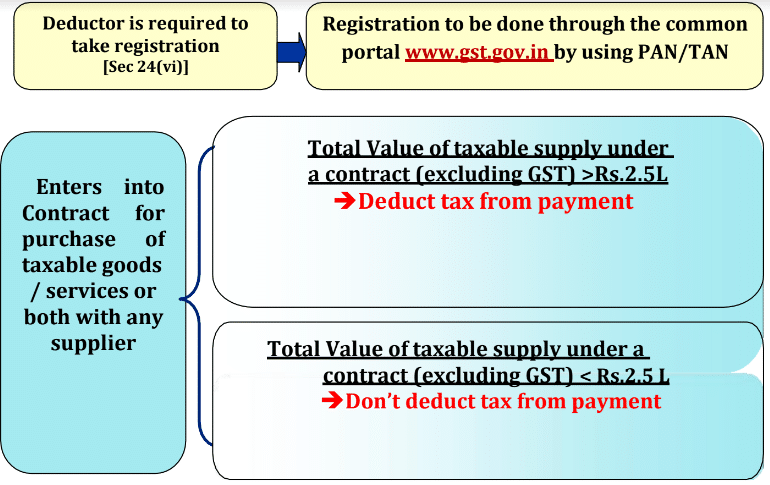

Tax is required to be deducted from the payment made / credited to a supplier, if the total value of supply under a contract in respect of supply of taxable goods or services or both, exceeds Rs. 2,50,000/- (Rupees two lakh and fifty thousand).

This value shall exclude the taxes leviable under GST (i.e. ‘Central tax’, ‘State tax’, ‘UT tax’, ‘Integrated tax’ & Cess).

3.1 Conditions for & amount of deduction:

⇒ Tax deduction is required if all the following conditions are satisfied ‑

a. Total value of taxable supply > Rs.2.5 Lakh under a single contract. This value shall exclude taxes & cess leviable under GST.

b. If the contract is made for both taxable supply and exempted supply, deduction will be made if the total value of taxable supply in the contract > Rs.2.5 Lakh. This value shall exclude taxes & cess leviable under GST.

c. Where the location of the supplier and the place of supply are in the same State/UT, it is an intra-State supply and TDS @ 1% each under CGST Act and SGST/UTGST Act is to be deducted if the deductor is registered in that State or Union territory without legislature.

d. Where the location of the supplier is in State A and the place of supply is in State or Union territory without legislature – B, it is an inter-State supply and TDS @ 2% under IGST Act is to be deducted if the deductor is registered in State or Union territory without legislature – B.

e. Where the location of the supplier is in State A and the place of supply is in State or Union territory without legislature B, it is an inter-State supply and TDS @ 2% under IGST Act is to be deducted if the deductor is registered in State A.

f. When advance is paid to a supplier on or after 01.10.2018 to a supplier for supply of taxable goods or services or both.

4. When tax deduction is not required to be made under GST:

Tax deduction is not required in following situations:

a) Total value of taxable supply <= 2.5 Lakh under a contract.

b) Contract value > Rs. 2.5 Lakh for both taxable supply and exempted supply, but the value of taxable supply under the said contract <= 2.5 Lakh.

c) Receipt of services which are exempted. For example services exempted under notification No. 12/2017 – Central Tax (Rate) dated 28.06.2017 as amended from time to time.

d) Receipt of goods which are exempted. For example goods exempted under notification No. 2/2017 – Central Tax (Rate) dated 28.06.2017 as amended from time to time.

e) Goods on which GST is not leviable. For example petrol, diesel, petroleum crude, natural gas, aviation turbine fuel (ATF) and alcohol for human consumption.

f) Where a supplier had issued an invoice for any sale of goods in respect of which tax was required to be deducted at source under the VAT Law before 01.07.2017, but where payment for such sale is made on or after 01.07.2017 [Section 142(13) refers].

g) Where the location of the supplier and place of supply is in a State(s)/UT(s) which is different from the State / UT where the deductor is registered.

h) All activities or transactions specified in Schedule III of the CGST/SGST Acts 2017, irrespective of the value.

i) Where the payment relates to a tax invoice that has been issued before 01.10.2018.

j) Where any amount was paid in advance prior to 01.10.2018 and the tax invoice has been issued on or after 01.10.18, to the extent of advance payment made before 01.10.2018.

k) Where the tax is to be paid on reverse charge by the recipient i.e. the deductee.

l) Where the payment is made to an unregistered supplier.

m) Where the payment relates to “Cess” component.

5. Illustrations of various situations requiring deduction of tax:

| Situations / Contracts | Deduction required YES / NO | Remarks |

| Finance Department is making a payment of Rs.3 Lakh to a supplier of ‘printing & stationery’. | Yes | Where the total contract value of taxable supply is more than Rs.2.5 Lakh deduction is mandatory. |

| Education Department is making payment of Rs.5 Lakh to a supplier of ‘printed books and printed or illustrated post cards’ where payment for books is Rs.2 Lakh and Rs.3 Lakh is for other printed or illustrated post cards. | Yes, deduction is required in respect of payment of Rs. 3 Lakh only i.e. for payment in respect of taxable supply. | Books are exempted goods; no deduction is required in respect of supply of books. However, payment involving ‘printed or illustrated post cards’ is for supply of taxable goods and value of such supply is > Rs.2.5 Lakh; so deduction is required. |

| Finance Department, is making payment of Rs.1.5 Lakh to a supplier of ‘car rental service’. | See Remarks | Deduction is mandatory in case the total value of taxable supply under the contract > Rs.2.5 Lakh irrespective of the amount paid. However, if the total value of supply under a contract is < Rs.2.5 Lakh, deduction is not required. |

| Health Department executed a contract with a local supplier to supply “medical grade oxygen” of Rs.2.6 Lakh (including GST) and is making full payment. | No | Total value of supply as per the contract is Rs.2.6 Lakh (including GST). Tax rate is 12%. So, taxable value of supply (excluding GST) stands at Rs.2.6L x 100/112 = Rs.2.32 L < Rs.2.5 Lakh Hence, deduction is not required. |

| Municipal Corporation of Kolkata purchases a heavy generator from a supplier in Delhi. Now, it is making payment of Rs.5 Lakh and IGST @18% on Rs.5 Lakh for such purchase. | Yes, deduction is required @2% | Deduction is required in case of inter-State supply and if the value of taxable supply under a contract exceeds Rs.2.5 Lakh. |

| Fisheries Department is making a payment of Rs.10 Lakh to a contractor for supplying labour for digging a pond for the purpose of Fisheries. | No | This supply of service is exempt in terms of Sl. No. 3 of notification No.12/2017 – Central Tax (Rate) dated 28.06.2017 and hence deduction is not required. |

| Municipality is making payment of Rs.5 Lakh to a supplier in respect of cleaning of drains where the value of supply of goods is not more than 25% of the value of composite supply. | No | This supply of service is exempt in terms of Sl. No. 3A of notification No.12/2017 – Central Tax (Rate) dated 28.06.2017 as amended by notification no. 2/2018- Central Tax (Rate) dated 25.01.2018 and hence deduction is not required. |

| Government school is making a payment of Rs.3 Lakh to a supplier for supply of cooked food as mid-day meal under a scheme sponsored by Central/State Government. | No | This supply of service is exempt in terms of Sl. No. 66 of notification No. 12/2017 – Central Tax (Rate) dated 28.06.2017 as amended and hence deduction is not required. |

| Health Department is making payment of Rs.10 Lakh to a supplier for supply of Hearing Aids. | No | This supply of goods is exempt in terms of Sl. No.142 of notification No. 2/2017 – Central Tax (Rate) dated 28.06.2017 as amended and hence deduction is not required. |

–

| Situation (in all cases taxable contract value is over Rs.2.5 Lakh) | Location of Supplier | Place of Supply | State of registration of recipient | Type of Supply | Tax | TDS deduction |

| Govt. of WB purchases taxable goods from a local supplier | Kolkata | Kolkata | West Bengal | Intra State | CGST+ SGST | Yes |

| Govt. of Punjab purchases taxable goods from a supplier in Delhi | Delhi | Punjab | Punjab | Inter State | IGST | Yes |

| Govt. of WB engages a contractor of Delhi for renovation of Bangla Bhawan in Delhi | Delhi | Delhi | West Bengal | Intra State in the State of Delhi | CGST+ SGST | N |

6. Valuation of supply for deduction of TDS and applicable rates with illustrations:

For the purpose of deduction of TDS, the value of supply shall exclude the taxes leviable under GST (i.e. ‘Central tax’, ‘State tax’, ‘UT tax’, ‘Integrated tax’ & Cess). Thus, no tax shall be deducted on ‘Central tax’, ‘State tax’, ‘UT tax’, ‘Integrated tax’ and cess component levied on supply. No deduction of tax and cess should also be made on the value of exempted goods or services or both even if the exempt and taxable supply are billed together.

NOTE: Suppose three separate contracts for supply are given to M/S ABC by the Health Department of the Government of West Bengal and the value of taxable supply is below Rs.2.5 Lakh in case of each contract though their combined value is more than Rs.2.5 Lakh; in such case no deduction is required to be made since value of taxable supply in neither of the contract exceeds Rs. 2.5 Lakh.

6.1 Rate of deduction of tax:

There are 4 types of taxes in GST – Integrated Tax (IGST), Central Tax (CGST) and State Tax (SGST) / Union territory Tax (UTGST).

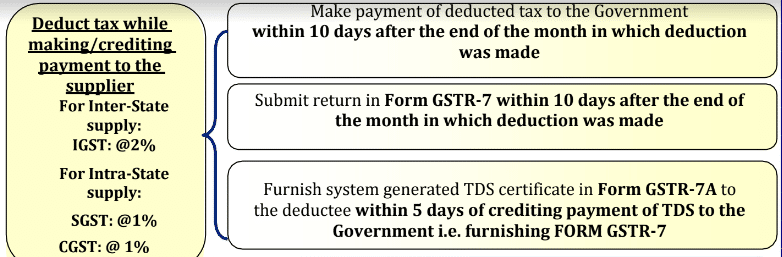

The deduction in case of intra-State supply (supply within a State) will be CGST & SGST (in case of Union territory without legislature, it will be CGST & UTGST), and the deduction in case of inter-State supply (supply from one State to another) will be IGST.

Rate of such deduction is @ 2% [i.e. 1% each on CGST & SGST/UTGST component] on the amount paid/credited in respect of intra-State supply & @ 2% [as IGST] on the amount paid/credited in respect of inter-State supply.

6.2 Illustration of various situations requiring determination of value of supply for deduction of tax:

6.2.1 Supplier is registered and contract value is excluding GST:

Example 1: Supplier X makes taxable supply worth Rs. 10,000/- to a Municipality where contract for supply is for Rs.15,00,000/-. The rate of GST is 18%. Supplier and the deductor are in the same State. Following payment is being made by this Municipality to X:

Rs. 10,000 (value of Supply) + Rs 900 (Central Tax) + Rs 900 (State Tax).

Value of supply = Rs.10,000/-

Tax to be deducted from payment:

Central Tax = 1% on Rs.10,000/- = Rs.100/- ; State Tax = 1% on Rs.10,000/- = Rs.100/-

Payment due to X after TDS as per GST provisions: Rs. 11600/-

6.2.2 Supplier is registered and contract value is inclusive of GST:

Example 2: Supplier Y of Mumbai makes taxable supply worth Rs. 10,000/- & exempted supply worth Rs. 20,000/- in an invoice/bill of supply to Finance Deptt. of GoI located in New Delhi where contract for supply is for Rs.6,00,000/- (Rs.2,60,000 for taxable supply including GST and Rs.3,40,000 for exempted supply). The rate of GST is 18%. Following payment is being made by GoI to Y: Rs.10,000/- (value of taxable Supply) + Rs.1,800 (Integrated Tax) + Rs.20, 000/- (value of exempted Supply).

Whether any deduction of tax is required?

Value of taxable supply in the contract= Rs.2,60, 000/- (including GST) Value of such contract excluding tax= 260000 x 100/118= Rs.220340/-

Since, the value of taxable supply in the contract does not exceed Rs.2.5 Lakh, deduction of tax is not required.

6.2.3 Supplier is registered under composition scheme:

Example 4: Supplier ZA is a person registered under the composition scheme in Jharkhand who makes taxable supply worth Rs. 10,000/- to a Local Authority of Jharkhand where value of taxable supply under the contract is for Rs.2, 55,000/-

Following payment is being made by the Local Authority of Jharkhand to ZA: Rs.10, 000/-

Value of taxable supply under the contract is Rs.2, 55, 000/- which is more than Rs.2.5 Lakh and hence deduction of tax is required.

7. Persons liable to deduct tax under GST Law:

As per the provisions of the GST Law, the following persons are mandatorily required to deduct TDS :-

(a) a department or establishment of the Central/ State Government; or

(b) local authority; or

(c) Governmental agencies; or

(d) such persons or category of persons as may be notified by the Government on the recommendations of the Council.

The following class of persons under clause (d) of section 51(1) of the CGST Act, 2017 has been notified vide notification No. 33/2017 – Central Tax dated 15.09.2017 :-

(a) an authority or a board or any other body,—

(i) set up by an Act of Parliament or a State Legislature; or

(ii) established by any Government,

with fifty-one percent or more participation by way of equity or control, to carry out any function;

(b) society established by the Central/ State Government or a Local Authority under the Societies Registration Act,1860;

(c) public sector undertakings.

Local authority:

Section 2(69): “local authority” means–

(a) a “Panchayat” as defined in clause (d) of article 243 of the Constitution;

(b) a “Municipality” as defined in clause (e) of article 243P of the Constitution;

(c) a Municipal Committee, a Zilla Parishad, a District Board, and any other authority legally entitled to, or entrusted by the Central Government or any State Government with the control or management of a municipal or local fund;

(d) a Cantonment Board as defined in section 3 of the Cantonments Act, 2006;

(e) a Regional Council or a District Council constituted under the Sixth Schedule to the Constitution;

(f) a Development Board constituted under article 371 of the Constitution; or

(g) a Regional Council constituted under article 371A of the Constitution.

8. Registration of deductor of tax in GST:

• The existing deductors of STDS/TCS under VAT Act will not be automatically migrated to GST.

• Section 24(vi) of the CGST Act, 2017 provides for compulsory liability for registration for the deductors of TDS.

• A deductor in GST will be required to get registered and obtain a GSTIN [Goods & Services Tax Identification Number] as a TDS deductor even if he is separately registered as a supplier.

• A deductor has to get himself registered through the portal www.gst.gov.in by using their PAN/TAN. The entire process is online.

8.1 Step by step process of registration of TDS Deductors in GST:

PART – I : Entering User credentials for Registration Application

1. Go to the GST Portal at www.gst.gov.in

2. Click on the “Services” Tab →Click on “Registration” →Select “New Registration”.

3. Find the box “I am a” which will capture your status as an applicant. Select “Tax Deductor” from the drop-down menu.

4. Look below for the options: I have a (a) PAN (b) TAN. Please select the option “TAN”.

5. Enter the TAN in the box below.

6. Now find the box “State” and select your State (e.g. West Bengal) from the drop-down Menu.

7. Select the applicable district (e.g. Howrah) from the drop- down Menu in the “District” box.

8. Find the box “Legal name of the Tax deductor”. Enter the name as mentioned in TAN. Please don’t deviate from such data.

9. Enter your e-mail address and Mobile Number in the respective boxes. Please ensure that this e-mail and mobile are regularly accessed by you. OTP for registration will be sent to these contacts only.

10. Enter the Captcha Code as displayed onscreen.

11. Click on the button “Proceed”.

12. Automatically you will be guided to the next page.

13. The system will also send 2 different OTPs. One to the Mobile Number and another to the e-mail id as entered by you.

PART – II : OTP Verification

1. Enter the individual OTPs sent to your e-mail id & the Mobile number in the respective boxes.

2. In case, you have not received the OTPs due to any reason, you may click on the link “Click here to resend the OTP”.

3. Click on the button “Proceed”.

4. A Temporary Reference Number (TRN) will be generated.

Please note this TRN is for further course of action.

5. Now, you have to fill up the rest of the details in the Registration Application against this TRN only.

6. Click on the button “Proceed” to leave this page.

7. This TRN will be valid for 15 days. So you can always come back to the system for filling up the rest of the details at any time within such 15 days. In case this TRN expires beyond 15 days, you will have to follow the steps as detailed in Part I and Part II all afresh.

PART – III : Filling up the registration Form : Entering TRN

1. Go to the GST Portal at www.gst.gov.in

2. Click on the “Services” Tab →Click on “Registration” →Select “TRN”.

3. Enter the TRN as you have noted down previously.

4. Enter the Captcha Code as displayed on screen.

5. Click on the button “Proceed”.

6. You will be guided to the next page.

PART – IV : Filling up the registration Form : OTP Verification

1. This time only 1 OTP will be sent to your e-mail id & the Mobile number.

2. Enter the OTP in the respective box.

3. In case, you have not received the OTPs due to any reason, you may click on the link “Click here to resend the OTP”.

4. Click on the button “Proceed”.

5. You will be guided to the “My saved Applications” page.

6. The link of your application for Registration as a Tax Deductor in Form GST REG 07 will be displayed on screen with the corresponding expiry date of 15 days.

7. Click on the blue coloured box with an icon of Pen under the field “Action” to proceed.

8. Now you will be guided to the main application form for filling up the details.

9. This will have 5 different tabs. Please ensure that all the fields in the individual tabs are duly selected.

PART – V : Filling up the registration Form : Tab 1 : Business Details

1. As per the GST Law, Business includes all activities undertaken by a Govt. Dept. or a Local Authority. So, the Business details as

mentioned in this Form will capture your Office details.

2. The Legal Name of Tax Deductor, e-mail address, Mobile No., TAN and Status as a Tax Deductor will be displayed on screen automatically as all these have already been entered by you.

3. Ignore the box “Trade Name”.

4. Select your Office type e.g. Govt. Dept./ Local Authority etc. from the drop down menu of the box “Constitution of Business”.

5. Select “Type of Government” as State or Central (as applicable) if you have entered your constitution as Govt. Dept.

6. Date of liability will be auto-populated. You need not worry even it shows as the current date because you will be liable to deduct TDS only from the day, Section 51 of the CGST/SGST Acts, 2017 is notified i.e. with effect from 01.10.2018. If you apply for registration after this date, you will be liable from the date of application for registration.

7. Enter the State Jurisdiction details by selecting the applicable “District” and “Sector/Circle/Charge/Unit” from the drop-down menu.

8. Enter the Center Jurisdiction accordingly. To know the Central Jurisdiction, you may click on the designated link given therein and find the appropriate data.

9. Click on “Save and Continue” to proceed to the next tab.

10. Once all the required data are filled up, you will find that the Tab:

Business Details will be displayed with a tick (√) mark.

PART – VI : Filling up the registration Form : Tab 2 : DDO Details

1. Enter the Personal details of the DDO in the first part of this page.

2. Here you will have to enter: (a) name of DDO, (b) Father’s name of DDO, (c) Date of Birth, (d) Mobile Number, (e) e- mail address, (f) Gender, (g) Telephone (landline) with STD Code.

3. Enter the Identity Information of the DDO in the second part of this page.

4. Here you will have to enter: (a) Designation of DDO, (b) PAN of DDO, (c) Aadhar Number (not mandatory)

5. Enter the Residential details of the DDO in the third part of this page.

6. Here you will have to enter: (a) Residential address of the DDO.

7. Now, upload a photograph of the DDO in JPEG format (file size max. 100kb)

8. Select the button “Also authorized signatory” as Yes.

9. Click on “Save and Continue” to proceed to the next tab.

10. Once all the required data is filled up, you will find that the Tab: DDO Details will be displayed with a tick (√) mark.

PART – VII : Filling up the registration Form : Tab 3 : Authorised Signatory Details

1. As you have already selected the button “Also authorized signatory” as Yesin the previous page, the data from DDO details will be autopopulated.

2. Click on “Save and Continue” to proceed to the next tab.

3. Once all the required data is filled up, you will find that the Tab:

Authorised Signatory Details will be displayed with a tick (√) mark.

PART – VIII : Filling up the registration Form : Tab 4 : Office AddressDetails

1. Enter the DDO’s Office Address details in the first part of this page.

2. Enter the Office Contact details in the second part of this page.

3. Select the nature of possession of premises from drop-down menu.

4. Now, select from the drop-down menu, a type of document you want to upload as an address proof.

5. Now upload such document accordingly either in PDF or JPEG format (file size max. 2mb)

6. Click on “Save and Continue” to proceed to the next tab.

7. Once all the required data is filled up, you will find that the Tab: Office Address Details will be displayed with a tick (√) mark.

PART – IX : Filling up the registration Form : Tab 5 : Verification

1. Select the Verification Check Box.

2. Select the DDO’s name (with TAN) from the drop-down menu of “Name of Authorised Signatory”.

3. Enter Place.

4. You can sign the application either with your DSC or with EVC.

5. Select the appropriate option and proceed accordingly.

6. In case you face any glitch regarding attaching your DSC, a

designated link for solution is provided in the page itself.

7. If you have entered all the details and have successfully submitted your properly signed application, the page will now display a success message and accordingly an Acknowledgement will be sent to you.

Now, the proper officer will process your application and your 15 digit GSTIN as a Tax Deductor will be generated.

9. Payment of TDS (provisions and procedure):

By nature, the method of depositing TDS under GST is very much similar with the method followed for VAT efs payment in VAT. In GST, there will be a single portal www.gst.gov.in for registration, payment and filing of Returns. This section to be State-specific and to be written by the State concerned in accordance with the respective Treasury Management System. The Centre has already issued necessary instructions.

9.1 Challan generation for depositing the deducted tax

The deductor has to generate a challan in the portal at www.gst.gov.in and deposit the tax so deducted through e-payment mode [Net Banking/Debit-Credit card/NEFT-RTGS] or OTC Mode [Cash/Cheque/DD].

For further details, circular No. 65/39/2018-DOR dated 14.09.2018 may be referred.

10. TDS return:

The filing the TDS Return in FORM GSTR-7 can be done both through the online mode in the GST portal as well as by using the offline tool.

10.1 TDS return submission procedure:

In the offline method, the deductor would be required to fill up the designated .xl file and upload the said file with signature validation.

Every registered TDS deductor is required to file a Return in FORM GSTR 7 electronically within 10th of the month succeeding the month in which deductions have been made to avoid payment of any late fee, interest. [Section 39(3) of the CGST Act, 2017 read with Rule 66 of the CGST Rules, 2017 refers]

Tax deposited by challan would get credited in the electronic cash ledger of the deductor. The liability of a deductor in FORM GSTR 7 has to be paid by him by debiting his electronic cash ledger.

The deductor shall furnish to the deductee a system generated certificate in FORM GSTR 7A mentioning therein the contract value, rate of deduction, amount deducted, amount paid to the Government and other related particulars. The said certificate is to be furnished within five days of crediting the amount so deducted to the Government i.e. within five days of furnishing return in FORM GSTR7.

The entire exercise has to be completed through www.gst.gov.in.

The deductee (i.e. the supplier) shall claim the credit of such deduction in his electronic cash ledger.

10.2 Time limit for filing the TDS Returns under GST:

The FORM GSTR-7 for a particular month has to be filed online within 10th of the month succeeding to the month in which deductions have been made.

11. Benefit of TDS to deductee and TDS certificate:

With the deduction of tax and submission of return in FORM GSTR 7 the amount deducted would be available in FORM GSTR 2A/4A of the registered deductee and the same would be credited in his electronic cash ledger. The deductee would be able to utilize this amount for discharging his tax liabilities.

12. Late fee, interest and penalty:

Provision for late fees for late filing of TDS Returns in GST

The provision of late Fees in respect of TDS in the GST is a twolayered provision.

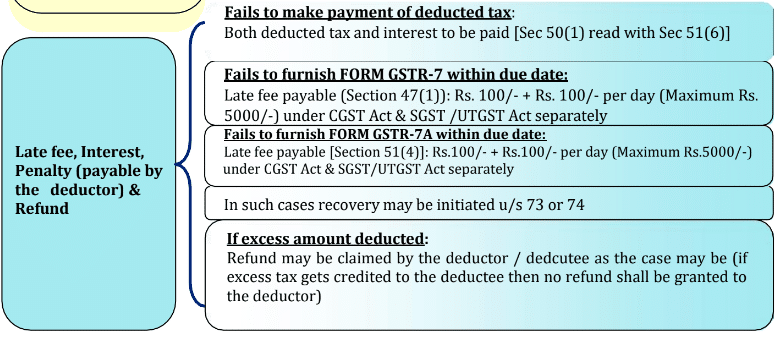

If the deductor fails to furnish the return in FORM GSTR-7 (under Section 39(3)) by the due date (i.e. within 10 days of the month succeeding the month in which deduction was made) he shall pay a late fee of Rs. 100/- per day under CGST Act & SGST/UTGST Act separately during which such failure continues subject to a maximum amount of Rs. 5000/- each under CGST Act & SGST/UTGST Act.

If any deductor fails to furnish the certificate of TDS deduction to the deductee [i.e. the supplier] within 5 days of crediting the amount so deducted to the Government (i.e. furnishing return in FORM GSTR7), the deductor shall pay a late fee of Rs. 100/- per day under CGST Act & SGST/UTGST Act separately from the day after the expiry of five day period until the failure is rectified, subject to a maximum amount of Rs.5000/- each under CGST Act & SGST/UTGST Act

13. Legal References

| Details | Sections of CGST/SGST Act, 2017 | Rules of CGST/SGST Rules, 2017 | GST Forms |

| Deduction of TDS, Persons liable to deduct, Conditions & Rate of deduction | Section 51 | Rule 66 | |

| Compulsory Liability of Registration for TDS deductors | Section 24(vi) | ||

| Application for registration | Section 25 | Rule 12(1) | GST REG-07 |

| Grant of Registration Certificate | Rule 12(2) | GST REG-06 | |

| Cancellation of Registration | Rule 12(3) read with Rule 22 | GST REG-08 | |

| Payment of TDS | Section 51(2) | Rule 85(4) | GST PMT-05 |

| Payment through GST Challan | Rule 87(2) & Rule 87(3) | GST PMT-06 | |

| Communication to Bank in case amount paid is debited but CIN not generated | Rule 87(8) | GST PMT-07 | |

| TDS Return | Section 51(5) read with Section 39(3) | Rule 66(1) | GSTR-07 |

| Issue of Certificate of deduction | Section 51(3) | Rule 66(3) | GSTR-7A |

| Late Fees (for late filing of GSTR-7) | Section 47(1) | ||

| Late Fees (for late furnishing of GSTR-7A) | Section 51(4) | ||

| Interest | Section 51(6) read with Section 50(1); Sec 20(xxv)of IGST Act read with section 51(6) & section 50(1) of the CGST/SGST Act | ||

| Penal provisions Demands & recovery | Section 51(7) read with Section 73 & Section 74 & Section 122(1)(v) and Section 20(xxv) & 4th proviso to Section 20 of IGST Act | Rule 142 | DRC 1 to DRC 8 |

| Refund | Section 51(8) read with Section 54 | ||

| Transitional Provisions | Section 142(13) |

14 FAQ on TDS under GST is as under:

Question 1: As a DDO I am deducting TDS from salary and also while making payment of other bills under Income Tax Act. Then why should I need to deduct TDS again?

Answer: TDS under Income Tax is different from TDS under GST. There was a provision of TDS under VAT Act also. TDS under the GST Law is different from the above. Deductions of tax under the GST Laws is required to be made wherever applicable while making payments to the suppliers/ vendors of goods or services or both under GST for taxable supply of goods or services or both.

Persons liable to deduct TDS under GST Laws

Question 2: Who are liable to deduct TDS?

Answer: All the DDOs of the (a) a department or establishment of the Central Government or State Government; (b) local authority; (c) Governmental agencies; (d) an authority or a board or any other body, -(i) set up by an Act of Parliament or a State Legislature; or (ii) established by any Government, with fifty-one percent or more participation by way of equity or control, to carry out any function; (e) a society established by the Central Government or the State Government or a Local Authority under the Societies Registration Act, 1860 (21 of 1860); (f) public sector undertakings.

Question 3: Describe the responsibilities of DDO in TDS under GST to get his/her office registered under GST?

Answer:

- To know the GSTIN of his office

- To be aware of the contract value

- To know when to deduct TDS under GST

- To know the nature of TDS (IGST or CGST & SGST/UTGST) to be deducted & the rate of tax

- To know the GSTIN of his/her vendors/suppliers

- To deduct TDS while making/crediting payment

- To generate CPIN while depositing the deducted tax

- To pay the deducted amount of TDS to the appropriate Govt. A/c

- To submit GSTR-7(Return) J. To generate GSTR-7A (TDS certificate for suppliers)

Registration requirement for TDS deductors & Procedure of Registration

Question 4: Does every Government office require to be registered under GST laws?

Answer: Yes, every Government office shall get itself mandatorily registered under GST. Here the role of DDO is very important as he is responsible for deducting tax while making/crediting payment under GST in applicable cases and, unless & until the process of registration is completed, the DDO will not be able to deduct any tax

Question 5: I am a DDO of a small Government Office. My office has not entered into any contract with any vendor whose taxable value of supply is more than Rs 2.5 Lakh in the recent past. Do I have to take GST registration for my office?

Answer: No. You are liable to register only when you make a payment on which tax is required to be deducted.

Question 6: Do I have to pay any Fees for obtaining a GST registration?

Answer: No fee is required to be paid for obtaining a GST Registration on the common portal.

Question 7: Is there any printed form for registration which I require to fill up?

Answer: No. The process of getting registration under GST is a fully online process. Registration should be done in the common portal www.gst.gov.in. There is no need to submit any hardcopy of any form or any document for Registration.

Question 8: Is there any need to upload any document to complete the registration process?

Answer: Yes, (i) a proof of address of the concerned office & (ii) a scanned photo of concerned DDO is required to be uploaded. A valid TAN is also needed.

Question 9: What types of documents are needed to be uploaded for address proof?

Answer: Scanned copy of either of the following will have to be uploaded: valid electricity bill or Municipality khata copy or property tax receipt or any legal ownership documents etc

Question 10: To submit my registration application do I always need a DSC?

Answer: One can use Electronic Verification Code for submission of the registration form in the common portal apart from DSC.

Question 11: How do I know that I have submitted the application form correctly? What is an ARN?

Answer: A pop-up message will appear that the form has been successfully submitted & an Acknowledgement Reference Number (ARN) will be sent to the registered mobile no & registered email address of the applicant after successful submission of Registration Application (FORM GST REG-07) online.

Question 12: Is this ARN called the GST registration No?

Answer: No. This ARN is generated only for a temporary period. Once FORM GST REG-07 is processed by the proper officer, the 15-digit GSTIN of the Tax Deductor will be generated. This GSTIN is the GST Registration No. of the applicant office.

Question 13: How do I know that GSTIN has been generated for my office or not?

Answer: Information will be given to the DDO in his registered email id as well as registered mobile no.

Question 14: After getting GSTIN what should I do?

Answer: DDO should update his DDO master details with the GSTIN in their respective DDO login in E-bill module of PFMS.

Question 15: As a DDO, I have to enter some personal information to get TDS registration. What will happen if I get transferred? Will I still be responsible for any lapse committed by the DDO who succeeds me?

Answer: Is true that the DDO is personally liable for any lapses regarding TDS deduction. But at the same time, the personal details of the DDO as entered in the Registration Form can always be amended; it is suggested that, the new DDO upon assuming of office should immediately amend such details. However the GSTIN of the deductor will remain unaltered.

Question 16: If the new DDO does not amend the details of his predecessor in office whether the ex-DDO would be liable for any lapse done by this new DDO?

Answer: No, the ex-DDO will not be liable for any lapse by his successor in office. A DDO is required to perform any responsibility in respect of TDS in GST either through a valid DSC (which is person specific) or through an EVC which would be sent to the registered mobile no as well as registered email id of the DDO only.

Situations when tax is required to be deducted in GST

Q17 Is there any threshold exceeding which tax is required to be deducted?

Answer: Yes. Tax is required to be deducted from the payment made/credited to a supplier, if the value of supply under a contract in respect of supply of taxable goods or services or both, exceeds Rs. 2,50,000/- (Rupees two lakh and fifty thousand). This value shall exclude the taxes leviable under GST (i.e. ‘Central tax’, ‘State tax’, ‘UT tax’, ‘Integrated tax’ & ‘Cess’).

Q18 Mr B, a DDO of ABC Office of the Government West Bengal needs to buy stationeries for his office from supplier Mr C. Should Mr B deduct tax under GST while making payment to Mr C?

Answer: Yes, Mr B is required to deduct tax while making / crediting payment to Mr C if value of taxable supply under a contract exceeds Rs 2.5 lakh

Situations when Tax is not required to be deducted in GST

Q19 Is there any threshold up to which GST needs not to be deducted?

Answer: Yes, GST need not to be deducted where the value of taxable supply under a contract does not exceed Rs 2.5 lakh.

Q20 As a deductor am I supposed to deduct GST where the taxable value of the contract entered with supplier Mr A is Rs 2.5 Lakh?

Answer: No. As the total value of taxable supply under the contract does not exceed Rs 2.5 Lakh the deductor is not liable to deduct tax under GST

Q.21 I have entered into a contract worth Rs. 10 lakh with a supplier XYZ prior to 01.10.2018. Now, I am making a payment of Rs.1.5 Lakh in respect of an invoice dated 25.10.2018 submitted by the supplier. Should I deduct tax while making payment of Rs.1.5 Lakh?

Ans: Yes. Tax is required to be deducted since the payment is being made after the effective date.

Q.22 I have entered into a contract worth Rs. 10 Lakh with a supplier XYZ prior to 01.10.2018. I have made a payment of Rs.3 Lakhs to him prior to 01.10.2018. Now, I am making payment of the balance amount of Rs.7 Lakh after 01.10.2018. Should I deduct tax on Rs.10 Lakh?

Ans: No. Tax cannot be deducted for any payment made prior to 01.10.2018. So deduction will be

made only in respect of Rs.7 Lakh

Q.23 I enter into a contract with a supplier ABC where the value of taxable supply is Rs.2 Lakh and payment of Rs.1 Lakh has been made on 15.10.2018. Now, on 20.10.2018 the contract value is revised from Rs.2 Lakh to Rs.6 Lakh. Am I liable to deduct any tax and if so, on which amount?

Ans: Yes, TDS shall have to be deducted on entire amount i.e. Rs. 6 lakhs while making remaining payment of Rs.5 Lakh. In other words, 12,000/- would be deducted when remaining payment of Rs.5 Lakh is made.

Q.24 Mr A. Roy, a DDO has purchased goods during May, 2018. He could not make payment for such purchase due to shortage of allotment. He is expected to receive allotment only in October, 2018. Is he liable to deduct TDS while making payment in the month of October considering that the purchase was made before October?

Ans: The tax payer is required to adjust the TDS amount to his liability relating to such invoices in the month in which goods are supplied. Therefore, TDS cannot be made for the amount paid in October but goods or services supplied before 30.09.2018.

Q.25 When should I not deduct tax under GST?

Ans: No deduction is required in respect of payment against–

- all services which are exempted as per principal notification No.12/2017 – Central Tax (Rate) as amended from time to time;

- all goods which are exempted as per principal notification No.2/2017 – Central Tax (Rate) as amended from time to time;

- When the goods and services are supplied prior to 30.09.2018 and payments are being made after 01.10.2018.

Valuation for deduction of tax with illustrations

Q.26 Mr Z, a supplier in West Bengal has issued a Tax Invoice of Rs. 11,800/- for supply of goods/services or both worth Rs. 10,000/- and GST of Rs. 1,800/- to Mr A of ABC office in West Bengal. What is the value of payment on which Mr A should deduct TDS during making payment to Mr Z? Calculate the amount payable to Mr Z.

Ans: For purpose of deducting of TDS, the value of supply is to be taken as the amount excluding the tax indicated on the invoice. This means TDS shall not be deducted on the CGST, SGST or IGST component of invoice.

In this case, TDS is to be deducted on Rs. 10,000/- and not on the full amount of Rs. 11,800/-.

Mr Z has issued a Tax Invoice of Rs. 11,800/- which comprises a GST component of Rs. 1,800/-. TDS in this case is to be deducted @ 2% (1% of CGST & 1% of SGST) on Rs. 10,000/-. Mr A will deduct Rs. 200/- which he will deposit in the proper Govt. A/c head. Mr A will pay Rs. 11600/- (11800/ – 200/-) = (i.e. Full Invoice Value – TDS amount) to Mr Z.

Nature of TDS & its Rate

Q.27 What is the different nature of supply & what is the rate of deduction?

Ans:

| Nature of Supply | Name of TDS | Rate of Tax |

| Location of the Supplier & Place of supply is in the same State /UT without any legislature | CGST | 1% |

| SGST / UTGST | 1% | |

| Location of the Supplier & Place of supply are in the different States | IGST | 2% |

Q.28 If Supplier A of Maharashtra supplies goods to ABC office in West Bengal, then tax is required to be deducted under which Act?

Ans: The concerned DDO needs to deduct IGST @2%.

Q.29 Health Department of WB receives a taxable service from MNO company of WB. What would be the nature of TDS to be deducted here & what would be the rate of deduction?

Ans: The DDO of the Health Department is liable to deduct TDS (1% CGST+1% SGST) while making payment to MNO Company as in this case the supplier or the vendor & the DDOs office (the place of supply) both are in West Bengal.

TDS Payment

Q.30 How can I discharge my TDS liability?

Ans: TDS liability can be discharged by debiting of Electronic Cash Ledger only at the time of filing return in FORM GSTR 7.

Q.31 Payment is made in respect of a single contract whose value of taxable supply is Rs.3.5 Lakh. Two bills amounting to Rs 1.5 lakh & Rs. 2 lakh respectively are passed for such payment. Since in respect of both the bills the amount paid does not exceed Rs. 2.5 lakh, I think that no tax is required to be deducted. Am I right?

Ans: No. Here the payments are being made against a single contract value of taxable supply exceeding Rs.2.5 Lakh. Here, the value of taxable supply in the contract is Rs. 3.5 lakh. So, the deductor should deduct TDS on each payment to the supplier in respect of the aforesaid contract.

Q.32 When will a DDO know that his liability for payment has been completed?

Ans: Electronic cash Ledger of the DDO will be credited when tax deducted at source is deposited in Government account. Payment of such liability (which is the tax deducted at source) shall have to be done by debiting of the electronic cash Ledger and such debit can be done while submitting FORM GSTR 7. So, unless the return in FORM GSTR 7 is submitted the payment liability of the DDO will not be completed.

Q.33 Can the deductee take action on the TDS credit declared by me?

Ans: Yes. After filing of return by deductors (DDOs) in FORM GSTR-7, the amount so deducted will be auto-populated in ‘TDS/TCS credit receipt’ table of respective suppliers. The supplier (deductee) has to accept or reject the amount so auto-populated in the table after logging on the portal. The accepted amount will be credited to Electronic cash ledger while rejected amount will be auto-populated in Amendment table of next month’s FORM GSTR-7 of the deductor.

Q.34 What will happen if the TDS credit entry is rejected by the deductee?

Ans: The rejected transactions in ‘TDS/TCS credit receipt’ table will be communicated back to the deductor who will download the auto-populated transactions and make necessary amendments in GSTIN or amount etc. in table 4 of FORM GSTR-7. The amended details will again be auto-populated in ‘TDS/TCS credit receipt” table. Supplier will take action comprising Accept/Reject the transactions. As usual, amount of accepted invoices will be credited to electronic cash ledger of the supplier.

Q.35 Is there any provision of refund to the deductor or the deductee arising on a/c of excess or erroneous deduction made under GST?

Ans: The refund to the deductor or the deductee arising on account of excess or erroneous deduction shall be dealt with in accordance with the provisions of section 54. Further no refund to the deductor shall be granted, if the amount deducted has been credited to the electronic cash ledger of the deductee.

TDS return

Q.36 Who are liable to file return (GSTR-7)?

Ans: Post 01.10.2018, DDOs deducting tax will be liable to file return in FORM GSTR-7 for the month in which such deductions are made.

Q.37 What is the need for filing a return when deposit of TDS has already been made?

Ans: Electronic cash Ledger of the DDO will be credited when tax deducted at source is deposited in Government account. Payment of such liability (which is the tax deducted at source) shall have to be done by debiting of the electronic cash Ledger and that can be done only while submitting FORM GSTR 7. So, unless the return in FORM GSTR 7 is submitted the payment liability of the DDO will not be treated as discharged.

Q.38 Mr S has deducted GST amounting to Rs 50,000/- in the month of Nov’18. He filed return on 16.12.2018. Is he liable to pay a late fee?

Ans: Yes he is liable to pay a late of Rs. 600/- at the rate of Rs 100/- per day for delay of 6 days (11.12.2018 – 16.12.2018). Maximum amount of late fee payable is capped at Rs.5,000/- Similar late fees is applicable under SGST Act / UTGST Act.

Q.39 During October, 2018, I have not deducted any amount of GST. Do I need to file return for the month of October?

Ans: The Deductor i.e. DDO is required to furnish a return in FORM GSTR-7 electronically for the month in which such deductions have been made in accordance with the provision of section 39(3) of the CGST/SGST Acts, 2017. Hence, submission of FORM GSTR-7 is not required for a month in which no deduction is made.

Q.40 How can a deductor file FORM GSTR-7?

Ans: FORM GSTR-7 can be filed on the GST Portal, by logging in the Returns Dashboard by the deductor.

The path is Services > Returns > Returns Dashboard.

Q.41 Is there any Offline Tool for filing Form GSTR-7?

Ans: Yes. FORM GSTR 7 return can be filed through offline mode also.

Q.42 Can the date of filing of FORM GSTR-7 be extended?

Ans: Yes, date of filing of FORM GSTR-7 can be extended by the Commissioner of State/Central tax through notification.

Q.43 What are the pre-conditions for filing FORM GSTR-7?

Ans: Pre-conditions for filing of FORM GSTR-7 are:

- Tax Deductor should be registered and should have a valid/active GSTIN.

- Tax Deductor should have a valid User ID and password.

- Tax Deductor should have an active & non-expired/ non-revoked digital signature (DSC) in case return is to be filed through DSC.

- Tax Deductor has made payment or credited the amount to the supplier’s account.

Q.44 What are the modes of signing FORM GSTR-7?

Ans: FORM GSTR-7 can be filed using DSC or EVC.

Q.45 Can I preview the FORM GSTR-7 before filing?

Ans: Yes, the preview of FORM GSTR-7 can be seen by clicking on ‘Preview Draft GSTR-7’ before filing on the GST Portal.

Q.46 What happens after FORM GSTR-7 is filed?

Ans: After FORM GSTR-7 is filed:

- ARN is generated on successful filing of the return in FORM GSTR-7.

- An SMS and an email are sent to the applicant on his registered mobile and email id.

Q.47 Can I file the complete FORM GSTR-7 using Offline Utility?

Ans: No. Filing can take place only online on the GST Portal.

The details of Table 3 and Table 4 can be prepared offline but remaining activities like payment and filing has to be completed on the portal only. Once the json file is uploaded on the GST Portal, one may continue to proceed to file. Liabilities will then be computed and after making payment, return can be filed.

Q.48 What are the features of FORM GSTR-7 Offline Utility?

Ans: The key features of FORM GSTR-7 Offline Utility are:

The FORM GSTR-7 details of Table 3 and 4 can be prepared offline, with no connection to Internet.

Most of the data entry and business validations are in built in the offline utility, reducing errors upon upload to GST Portal.

Q.49 From where can I download and use the FORM GSTR-7 Offline Utility in my system?

Ans: Following steps are required to be performed to download and open the FORM GSTR-7 Offline Utility in your system from the GST Portal:

1. Access the GST Portal: www.gst.gov.in.

2. Go to Downloads > Offline Tools > GSTR7 Offline Utility option and click on it

3. Unzip the downloaded Zip file which contain GSTR7_Offline_Utility.xls excel sheet.

4. Open the GSTR7_Offline_Utility.xls excel sheet by double clicking on it.

5. Read the ‘Read Me’ instructions on excel sheet and then fill the worksheet accordingly.

Q.50 Do I need to login to GST Portal to download the FORM GSTR-7 Offline Utility?

Ans: No. One can download the FORM GSTR-7 Offline Utility under ‘Download’ section without logging in to the GST Portal.

Q.51 Do I need to login to GST Portal to upload the generated JSON file using FORM GSTR-7 Offline Utility?

Ans: Yes. You must login in to the GST Portal to upload the generated JSON file using FORM GSTR- 7 Offline Utility.

Q.52 What are the basic system requirements/ configurations required to use FORM GSTR-7 Offline Tool?

Ans: The offline functions work best on Windows 7 and above and MS EXCEL 2007 and above.

Q.53 Is Offline utility mobile compatible?

Ans: As of now FORM GSTR-7 Offline utility cannot be used on mobile. It can only be used on desktop/laptops.

Q.54 How many TDS details of the suppliers can I enter in the offline utility?

Ans: One can enter maximum 10,000 rows of TDS details of the suppliers in the offline utility.

Q.55 I am a tax deductor. I’ve made payment for four different products to one of my suppliers. Shall I report each payment in four different rows of the offline utility?

Ans: No. Row with a duplicate GSTIN is not allowed in the utility. One should report the whole amount in one row only. All the payments are required to be added and one single consolidated amount has to be entered in the “Amount paid to deductee on which tax is deducted ” column.

Q.56 I have mistakenly entered rows with the same GSTIN. Should I use the “Delete” option from the dropdown of “Action” column to delete these rows?

Ans: No, the incorrect data has to be deleted in the utility manually using the “Delete” button of the keyboard.

Add and Delete options of the “Action” column are meant for adding or deleting data in the GST portal. Delete option is required to be ignored while preparing FORM GSTR-7 for first- time upload, and for the subsequent uploads it can be used only to delete those particular rows from the already-uploaded data on the portal.

Q.57 Can I enter negative or decimal amounts in the offline utility?

Ans: No, any negative value cannot be entered in the utility. However, decimal values can be entered. All decimal values would be rounded off to two decimal places. But, total liability will be rounded off to whole number.

Q.58 I’ve uploaded GSTR-7 JSON File and it was processed without error. Do I need to download the generated file?

Ans: No, it is not necessary to download the GSTR-7 JSON File processed without error. One can download it only if he wants to update, add or delete the details added previously. One can download the uploaded file for record if so required

Interest, Penalty & Late Fee

Q.59 Mr A, a DDO has submitted return for the month of November upon payment of liability as shown in such return on 11.12.2018. Is he liable to pay interest?

Ans: Mr. A has to pay interest for one day as return is to be filed by 10th December, 2018.

Q.60 Mr X has deducted Rs 1 lakh of TDS in Nov’18. He deposits Rs 70,000/- on 10.12.2018 & the rest of Rs 30,000 on 30.01.2019. He submits the return in FORM GSTR 7 on 28.02.2019. Has he incurred any liability to pay late fee or interest? Is he liable to pay any penalty?

Ans: Electronic Cash Ledger of the DDO is credited on 10.12.2018 and 30.01.2019 with Rs. 70,000/- and Rs. 30, 000/- respectively on account of deposit of TDS of Rs 70,000/- on 10.12.2018 & Rs 30,000 on 30.01.2019.

Since return in FORM GSTR 7 for the month of November, 2018 is filed on 28.02.2019 and he discharges his payment liability of tax so deducted by debiting his electronic cash ledger as well on this date only, therefore, late fee of 80 days (11.12.2018 to 28.02.2019) have to be paid under CGST and SGST. The amount of late fee will be restricted to Rs. 5000/- (upper limit provided in the Act). Interest has also to be paid for the delay. Penalty is also payable by a DDO if he fails to deduct the tax in accordance with the provisions of sub-section (1) of section 51, or deducts an amount which is less than the amount required to be deducted under the said sub-section, or where he fails to pay to the Government under sub-section (2) of section 51 [section 122(v) refers]. He is liable to penalty of Rs.1,00,000/-.

TDS Certificate &Benefit of TDS to the deductee

Q.61 As a DDO I have deducted tax while making payment to various Vendors. I have deposited the amount in the appropriate Government A/c & also filed return within stipulated time. Have I discharged all my liabilities relating to TDS?

Ans: No. A system generated TDS certificate in FORM GSTR-7A mentioning therein the value on which tax is deducted , and amount of tax deducted and other related particulars shall be available for download from the portal by deductee.

Q.62 How can a supplier download the TDS certificate in FORM GSTR 7A?

Ans: TDS certificate can be downloaded by access the www.gst.gov.in URL and using the following path: Login to the GST Portal with valid credentials. Navigate to Services > User Services > View/Download Certificates option.

Q.63 How many TDS Certificates are issued per GSTIN?

Ans: A single TDS certificate is issued per GSTIN per FORM GSTR-7 return filed by deductor.

Q.64 Is the signature of Tax Deductor required in TDS Certificate?

Ans: FORM GSTR-7A is system generated TDS certificate; signature of Tax Deductor is not required.

Q.65 Do I as a taxpayer have to file FORM GSTR-7A?

Ans: No, a tax payer (deductee) is not required to file FORM GSTR-7A.

Q.66 Can I as a taxpayer (Deductor or Deductee) download and keep a copy of my TDS Certificate for future reference?

Ans: Yes, TDS Certificate can be viewed and/or downloaded in post-login mode on the GST portal.

Q.67 Being a deductor do I have to fill any form to generate FORM GSTR 7A? How can I view Form GSTR-7A?

Ans: No, a deductor is not required to fill up any separate form for generation of FORM GSTR7A. FORM GSTR 7A shall be generated if return in FORM GSTR 7 is filed. To view Form GSTR-7A, perform following steps:

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the GST Portal with valid credentials.

3. Click the Services > User Services > View/Download Certificatescommand.

Disclaimer: This Standard Operating Procedure (SOP) is clarificatory in nature and is not meant for legal interpretation of provisions of relevant Acts and rules.

Download Complete FAQ, SOP and Ready Reckoner on TDS under GST

Also refer GST TCS FAQs by CBIC released : Download

Pingback: TaxHeal - GST and Income Tax Complete Guide Portal