Instructions for filling ITR-4 SUGAM A.Y. 2017-18

Download ITR-4 SUGAM AY 2017-18

General Instructions

These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act, 1961 and the Income tax Rules, 1962.

1. Assessment Year for which this Return Form is applicable

This Return Form is applicable for assessment year 2017-18 only, i.e., it relates to income earned in Financial Year 2016-17..

2. Who can use this Return Form

This Return Form is to be used by an individual/ HUF/ Partnership Firm whose total income for the assessment year 2017-18 includes:-

(a) Business income where such income is computed in accordance with special provisions referred to in sections 44AD and 44AE of the Act for computation of business income; or

(b) Income from Profession where such income is computed in accordance with special provisions referred to in sections 44ADA; or

(c) Salary/ Pension; or

(d) Income from One House Property (excluding cases where loss is brought forward from previous years); or

(e) Income from Other Sources (excluding Winning from Lottery and Income from Race Horses).

Note 1: The income computed shall be presumed to have been computed after giving full effect to every loss, allowance, depreciation or deduction under the Income-tax Act.

Note 2: Further, in a case where the income of another person like spouse, minor child, etc. is to be clubbed with the income of the assessee, this Return Form can be used only if the income being clubbed falls into the above income categories.

3. Who cannot use this Return Form

SUGAM cannot be used in following cases

(a) Income from more than one house property; or

(b) Income from Winnings from lottery or income from Race horses; or

(c) Income under the head “Capital Gains”, e.g. Short-term capital gains or long-term capital gains from sale of house, plot, shares etc.; or

(d) Income taxable under section 115BBDA; or

(e) Income of the nature referred to in section 115BBE; or

(f) Agricultural income in excess of ₹5,000; or

(g) Income from Speculative Business and other special incomes; or

(h) Income from an agency business or income in the nature of commission or brokerage; or

(i) Person claiming relief of foreign tax paid under section 90, 90A or 91; or

(j) Any resident having any asset (including financial interest in any entity) located outside India or signing authority in any account located outside India; or

(k) Any resident having income from any source outside India.

4. SUGAM form is not mandatory

SUGAM Business Form shall not apply at the option of the assessee, if –

(i) the assessee keeps and maintains all the books of account and other documents referred to in section 44AA in respect of the business or profession.

(ii) the assessee gets his accounts audited and obtains a report of such audit as required under section 44AB in respect of the business or profession. In the above scenarios, Regular ITR-3 or ITR-5, as the case may, should be filed and not SUGAM.

5. Annexure-less Return Form

No document (including TDS Certificate) should be attached to this Return Form. All such documents enclosed with this Return Form will be detached and returned to the person filing the return.

6. Manner of filing this Return Form

This Return Form can be filed with the Income-tax Department in any of the following ways–

(i) By furnishing the return in a paper form;

(ii)By furnishing the return electronically under digital signature;

(iii)By transmitting the data in the return electronically under electronic verification code;

(iv)By transmitting the data in the return electronically and thereafter submitting the verification of the return in Return Form ITR – V;

NOTE: Where the Return Form is furnished in the manner mentioned at 6(iv), the assessee should printout two copies of Form ITR – V;

In case of firm, (i) is not applicable.

One copy of ITR – V; duly signed by the assessee, has to be sent by post to – Post Bag No. 1, Electronic City Office, Bengaluru— 560 100, Karnataka. The other copy may be retained by the assessee for his record.

Only the following persons have an option to file return in paper form:-

(i) an individual of the age of 80 years or more at any time during the previous year; or

(ii) an individual or HUF whose income does not exceed five lakh rupees and no refund is claimed in the return of income.

7. Filling out the acknowledgment

Only one copy of this Return Form is required to be filed where the Return Form is furnished in the manner mentioned at 6(i). The acknowledgment/ ITR-V should be duly filled.

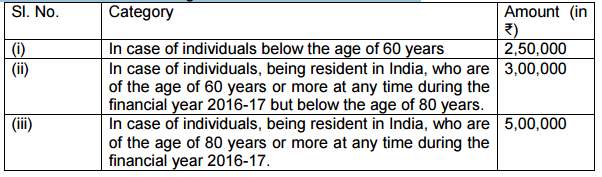

8. Obligation to file return

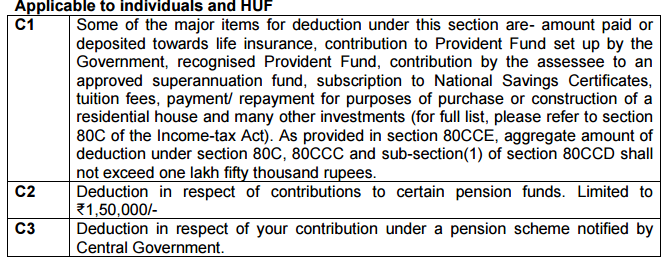

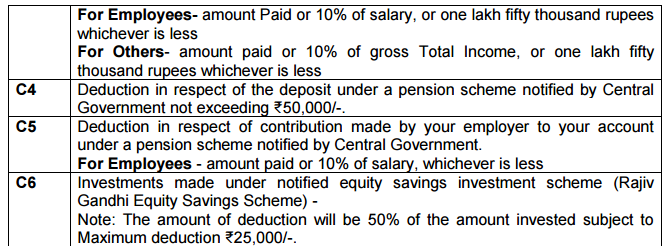

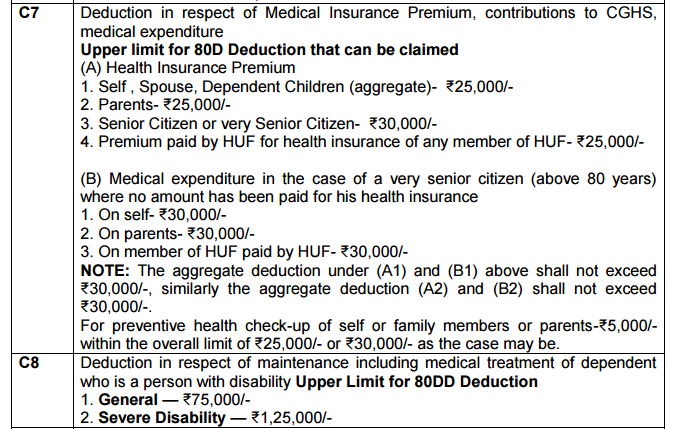

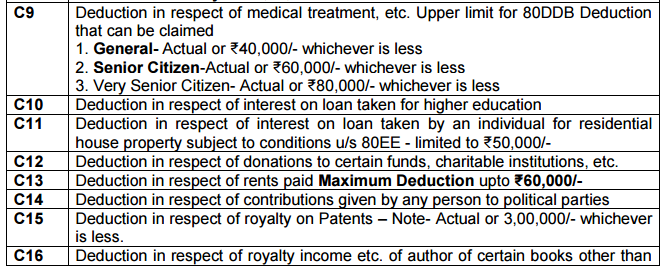

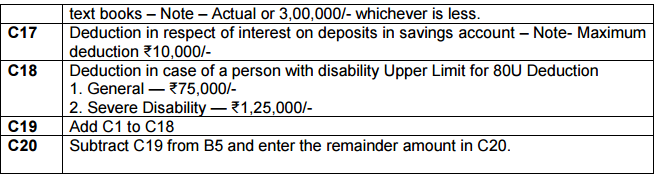

Every individual or HUF whose total income before allowing deductions under Chapter VI-A of the Income-tax Act, exceeds the maximum amount which is not chargeable to income tax is obligated to furnish his return of income. The deductions under Chapter VI-A are mentioned in Part C of this Return Form. The maximum amount not chargeable to income tax in case of different categories of individuals is as follows:-

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE.

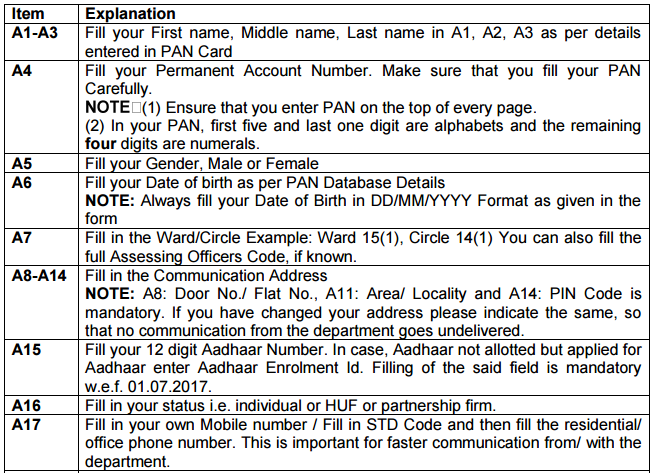

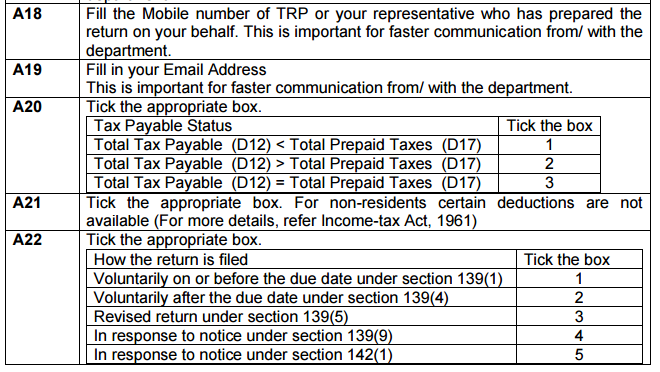

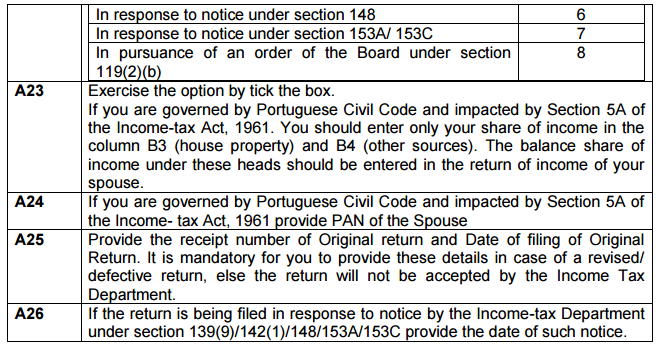

Item by Item Instructions

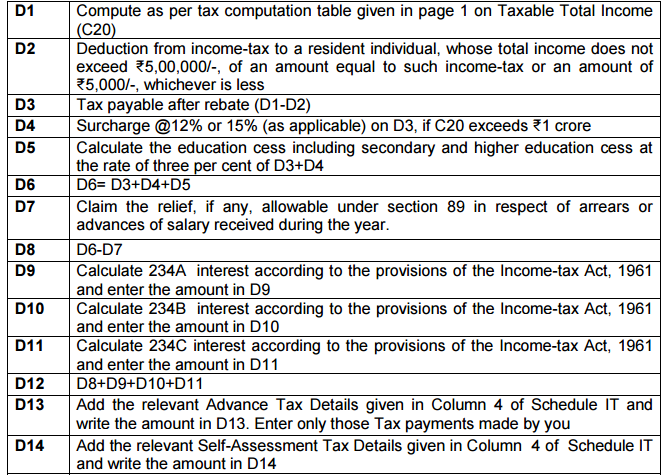

Tax Computation Table

A In case of individual or HUF

(i) In case of every individual (other than resident individual who is of the age of 60 years or more at any time during the financial year 2016-17) or HUF –

(ii) In case of resident individual who is of the age of 60 years or more but less than 80 years at any time during the financial year 2016-17-

(iii) In case of resident individual who is of the age of 80 years or more at any time during the financial year 2016-17-

(B) In case of a firm tax is to be calculated at flat rate of 30% of taxable income.

Verification

Please complete the Verification Section and Sign in the box given. Without a valid signature, your return will not be accepted by the Income-tax Department.

TRP Details

This return can be prepared by a Tax Return Preparer (TRP) also in accordance with the Tax Return Preparer Scheme, 2006 dated 28th November, 2006. If the return has been prepared by him, the relevant details have to be filled by him and the return has to be countersigned by him in the space provided in the said item.

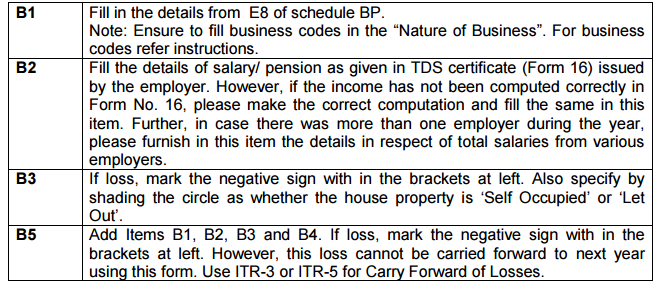

Sch BP

Sch AL

(i) This Schedule is to be filled by individuals and HUFs giving details of properties held by the assessee and the corresponding liabilities. It is mandatory if your total income exceeds ₹50 lakh.

(ii) The assets to be reported will include land, building (immovable assets); financial assets viz. bank deposits, shares and securities, insurance policies, loans and advances given, cash in hand and jewellery, bullion, vehicles, yachts, boats, aircraft etc. (movable assets) and interest held in the asset of a firm or association of persons (AOP) as a partner or member thereof.

(iii) In the case of non-resident and resident but not ordinarily resident, the details of assets located in India are to be mentioned.

(iv) For the purpose of Sl.No.(1)(i) under item B, jewellery includes.-

(a) Ornaments made of gold, silver, platinum or any other precious metal or any alloy containing one or more of such precious metals, whether or not containing any precious or semi-precious stone, and whether or not worked or sewn into any wearing apparel;

(b) Precious or semi-precious stones, whether or not set in any furniture, utensil or other article or worked or sewn into any wearing apparel.

(v) The amount in respect of assets to be reported will be:-

(a) the cost price of such asset to the assessee; or

(b) where wealth-tax return was filed by the assessee and the asset was forming part of the wealth-tax return, the value of such asset as per the latest wealth-tax return in which it was disclosed as increased by the cost of improvement incurred after such date, if any.

(vi) In case the asset became the property of the assessee under a gift, will or any mode specified in section 49(1) and not covered by (v) above:-

(a) the cost of such asset to be reported will be the cost for which the previous owner of the asset acquired it, as increased by the cost of any improvement of the asset incurred by the previous owner or the assessee, as the case may be; or.

(b) in case where the cost at which the asset was acquired by the previous owner is not ascertainable and no wealth-tax return was filed in respect of such asset, the value may be estimated at the circle rate or bullion rate, as the case may be, on the date of acquisition by the assessee as increased by cost of improvement, if any, or 31st day of March, 2017:

Previous owner shall have the meaning as provided in Explanation to section 49(1) of the Act.

Sch IT

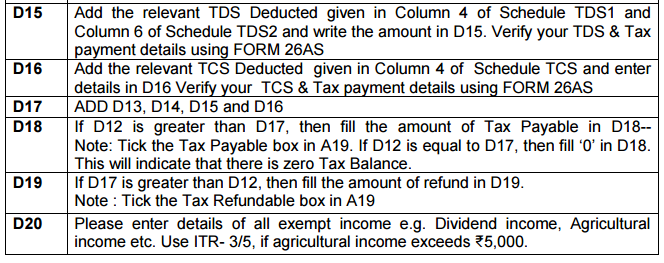

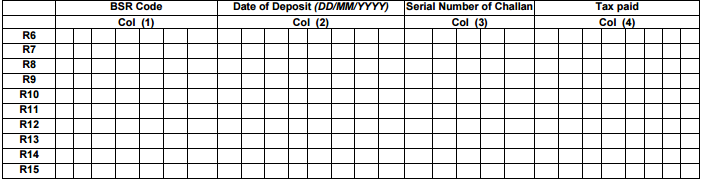

Please enter details of tax payments, i.e., advance tax and self-assessment tax made by you.

NOTE: If you have more than Five Self-Assessment and Advance Tax Details to be entered, then fill Supplementary Schedule IT and attach the same with the return.

NOTE: If you have more than Five Self-Assessment and Advance Tax Details to be entered, then fill the following table and tear and attach the same with the return (in case return is filed in paper form):

Sch TCS .

Please furnish the details of Tax collected at source. Note: If you have more than three TCS Details to be entered, then fill supplementary Schedule TCS and attach the same with the return

Sch TDS 1

Please furnish the details in accordance with Form 16 issued by the employer(s) in respect of salary income. Further in order to enable the Income Tax Department to provide accurate, quicker and full credit for taxes deducted at source, the taxpayer must ensure to quote complete details of every TDS transaction. If you have more than three Form 16 Details to be entered, then fill Supplementary Schedule TDS1 and attach the same with the return.

Sch TDS 2

(i)Please furnish the details in accordance with Form 16A issued by a person in respect of interest income and other sources of income.

(ii) All the tax deductions at source made in the current financial year should be reported in the TDS schedule.

(iii) “Unique TDS Certificate Number”. This is a six digit number which appears on the right hand top corner of those TDS certificates which have been generated by the deductor through the Tax Information Network (TIN) Central System.

(iv) “Deducted Year” means in which tax has been deducted. In this column fill up the four digits of relevant financial year. For example, if the deduction has been made by the deductor in the financial year 2016-17 fill up 2016 in the designated space.

(v) Enter the amount of TDS deducted which is claimed in this return of income. For example, if any income is not chargeable to tax in this year then the corresponding TDS deducted on such income, if any, will be allowable in the year in which such income is chargeable to tax.

(vi) If you are governed by Portuguese Civil Code and part of income is chargeable in your hands and part of it in the hands of your spouse, then enter in this column only part of TDS corresponding to part income chargeable in your hands.

Note: If you have more than four Form 16A Details to be entered, then fill supplementary Schedule TDS2 and attach the same with the return.