[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

(DEPARTMENT OF REVENUE)

(CENTRAL BOARD OF DIRECT TAXES)

NOTIFICATION

New Delhi, the 24 th June, 2016

INCOME-TAX

S.O. 2196 (E).— In exercise of the powers conferred by clause (ii) of sub-section (7) of section 206AA, read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax ( 17th Amendment) Rules, 2016.

(2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Income-tax Rules, 1962 (hereafter referred to as the said rules), after rule 37BB, the following rule shall be inserted, namely :-

“37BC. Relaxation from deduction of tax at higher rate under section 206AA.-

(1) In the case of a non-resident, not being a company, or a foreign company ( hereafter referred to as ‘the deductee’) and not having permanent account number the provisions of section 206AA shall not apply in respect of payments in the nature of interest, royalty, fees for technical services and payments on transfer of any capital asset, if the deductee furnishes the details and the documents specified in sub-rule (2) to the deductor.

(2) The deductee referred to in sub-rule (1), shall in respect of payments specified therein, furnish the following details and documents to the deductor, namely :-

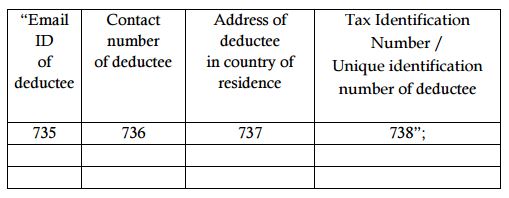

(i) name, e-mail id, contact number;

(ii) address in the country or specified territory outside India of which the deductee is a resident;

(iii) a certificate of his being resident in any country or specified territory outside India from the Government of that country or specified territory if the law of that country or specified territory provides for issuance of such certificate;

(iv) Tax Identification Number of the deductee in the country or specified territory of his residence and in case no such number is available, then a unique number on the basis of which the deductee is identified by the Government of that country or the specified territory of which he claims to be a resident.

3. In the said rules, in Appendix II, in Form No. 27Q,-

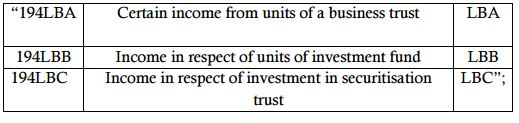

(a) in the second line, after the figures and letters “194LB”, the figures and letters “194LBA, 194LBB,194 LBC” shall be inserted;

(b) in the Annexure,-

(I) in the Table,-

(i) in the column 717, in the column heading, after the letters and words “PAN of the deductee”, the brackets, words and figure “[ see Note 5]” shall be inserted;

(ii) after column 734, the following shall be inserted, namely :—

(II) in the Notes below the Table,-

(A)in point 4, in the Table, after entry 194LB, the following shall be inserted, namely:—

(B) after point 4 and below the Table, the following point shall be inserted namely:—

‘5. In case of deductees covered under rule 37BC, “PAN NOT AVAILABLE” should be mentioned.’.”

[Notification No. 53 /2016, F.No.370 142/16/2016-TPL]

(LAKSHMI NARAYANAN)

UNDER SECRETRAY (TAX POLICY AND LEGISLATION)

Note: The principal rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (ii) vide notification number S.O.969( E), dated the 26th March, 1962 and last amended vide notification number S.O.2179(E), dated the 22nd June 2016.

Related Post

- TDS as per DTAA if No PAN with NRI

- Quoting PAN Mandatory for Transaction: Rule 114B of Income tax

- Rate of TCS on Cash sales if Buyer PAN not available

- FORM NO 60 Download (No PAN and Rule 114B transaction)

- How to Apply PAN Card (Permanent Account Number )

- Duplicate PAN Card Procedure

- Employer not liable to deduct TDS @ 20% for non furnishing of PAN by Employees